Key Figures and Discoveries:

- Stablecoin supply grew over 59% in 2024, reaching 1% of the U.S. dollar supply but lost 13.5% in weight within the total crypto market cap.

- The annual stablecoin transfer volume reached $27.6 trillion, surpassing a combined volume of Visa and Mastercard in 2024 by over 7.68%.

- 70% of stablecoin transaction volume in 2024 was related to bot activity. In Solana and Base networks bot transactions accounted for 98% of the volume.

- Yield-bearing stablecoins now account for over 3% of the stablecoin market, and became a major driver behind a 414% surge in market cap of tokenized treasuries.

- Ethereum and Tron dominance in hosting stablecoins decreased from 90% to 83%, with Base, Solana, Arbitrum, and Aptos capturing most of this share.

- Stablecoins registered over $25.8 trillion in aggregated trading volume in 2024, continuing to gain market share over fiat-to-crypto trading.

- The average daily trading volume among stablecoins soared by over 237% in a year. However, the relative weight of stablecoin volume declined compared to total crypto volumes due to increased adoption of derivative products.

- USDT accounted for 79.7% of stablecoin trading volume on average, and strengthened its positions amid surged stablecoin reserves on centralized exchanges.

Introduction

While memecoins and AI have been among the most profitable crypto narratives in 2024, stablecoins have emerged as one of the most impactful, serving as a major driver of crypto adoption. This adoption has accelerated not only among retail investors, who increasingly use stablecoins for savings and payments, but also among financial institutions.

While PayPal began using its proprietary stablecoin for business transactions, other fintech companies have been catching up, with Stripe acquiring a stablecoin issuance platform, Ripple launching RLUSD, and Robinhood, Kraken, and Galaxy collaborating to create a global stablecoin network. This trend continues to gain momentum, as Revolut considers developing its own stablecoin and Visa introduces a platform to help banks manage their stablecoins.

All of this suggests that stablecoins are set to become an even fiercer battlefield between traditional and crypto-native companies. To assess what to expect from stablecoins in 2025, we examined the current state of the sector and its developments over the past year.

Methodology

To provide an in-depth and comprehensive analysis of stablecoin trends, this report utilizes a diverse range of trusted sources, including DeFiLlama, Artemis, The Block, Visa/Allium, CoinGecko, CryptoQuant, Checkonchain, and GrowThePie. These platforms provided key metrics on stablecoin supply, on-chain activity, and trading dynamics to validate market developments across fiat-backed, crypto-backed, algorithmic, and yield-bearing stablecoins.

In addition, the report incorporated a comparative analysis of network-specific dynamics, capturing the evolving roles of Layer 1 (L1) and Layer 2 (L2) networks in the stablecoin ecosystem. To accurately reflect genuine transaction activity, this analysis highlights both total unfiltered data and adjusted metrics that exclude internal smart contract transactions, internal exchange transfers, and bot-driven activity.

Supply by Categories

Total Supply&

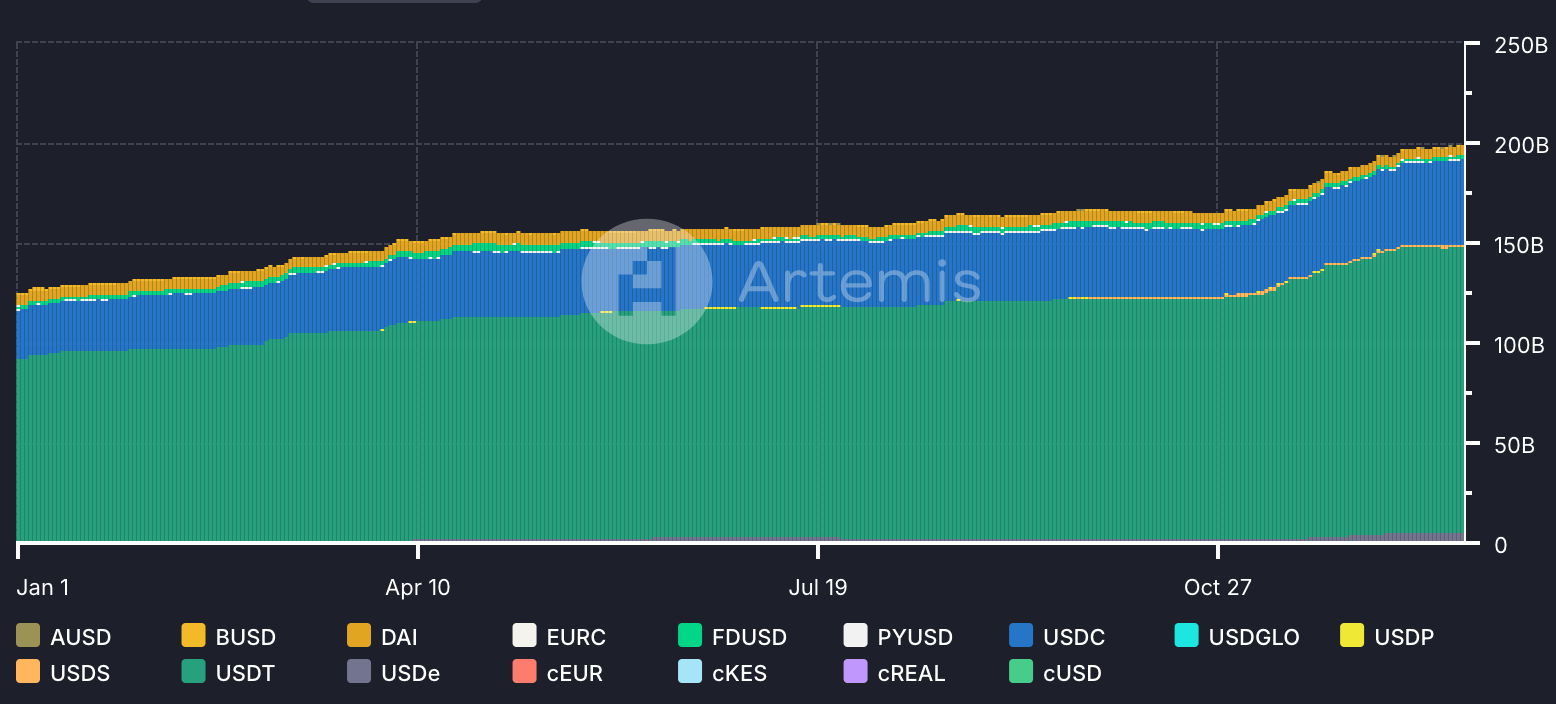

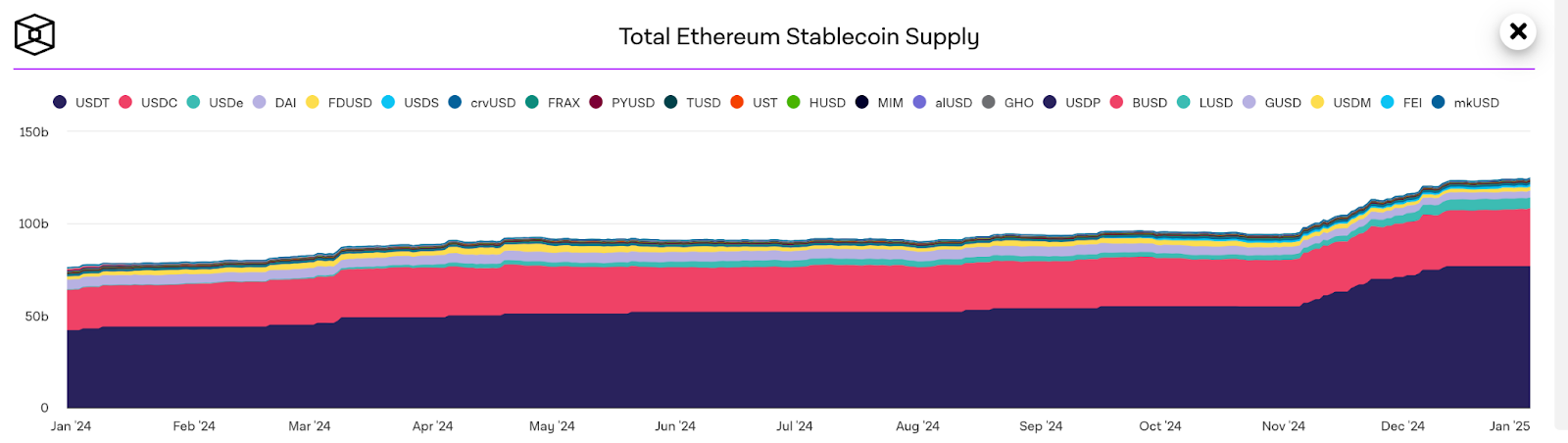

In 2024, the total stablecoin supply increased by over 59%, reaching a new all-time high in September, and surpassing $200 billion. Stablecoins now account for around 1% of the total U.S. dollar supply, up from 0.63% at the beginning of 2024.

The sector showed consistent increase throughout the year, accelerating its pace in Q1 and Q4 to complement the wider market growth during these periods. Despite this, the relative weight of the stablecoin sector to the total crypto market cap decreased from 8% to 6% during the year, as other sectors within the crypto market experienced higher increase.&

Chart: Total Stablecoin Supply Trends in 2024

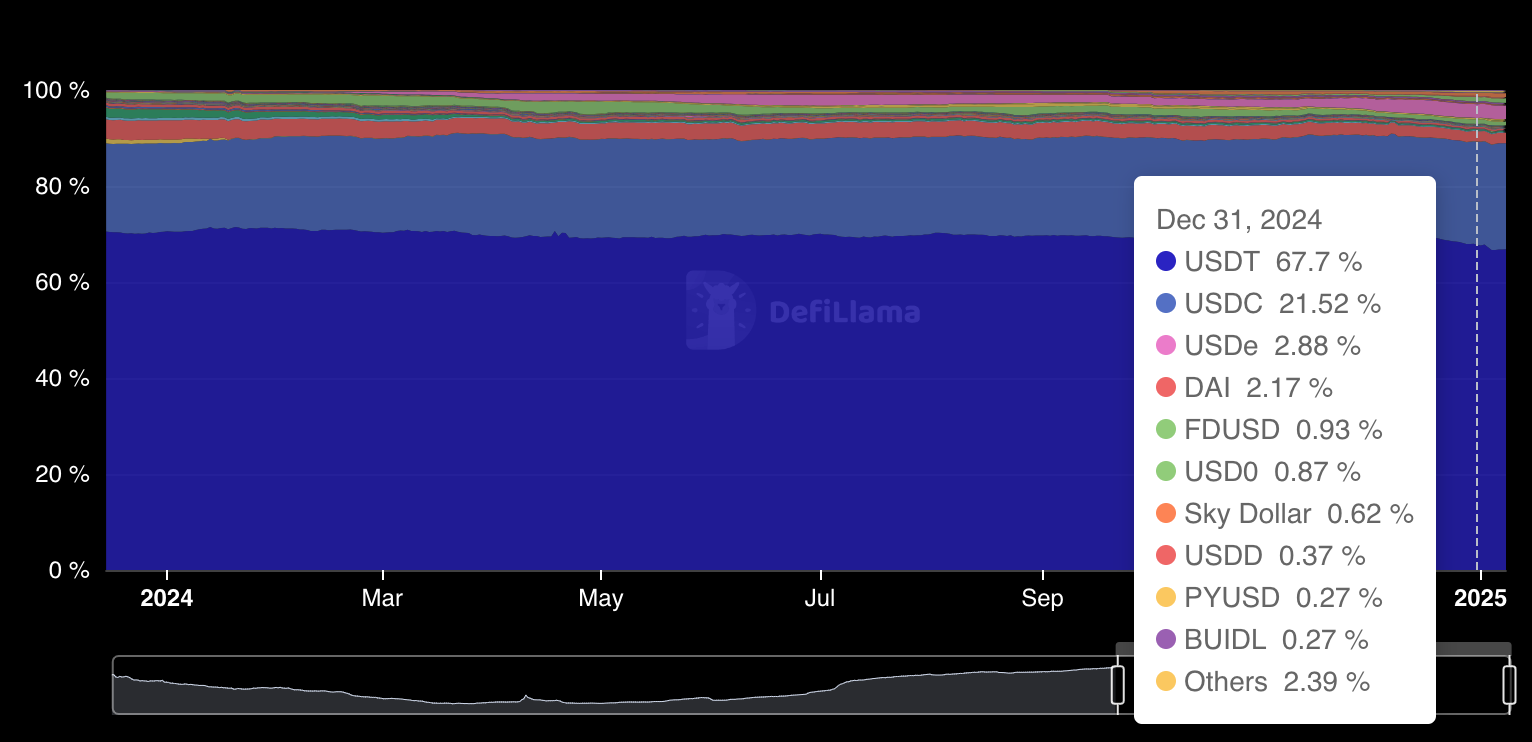

The supply distribution across top stablecoins has seen slight changes, with USDT remaining a dominant stablecoin, but its share in total supply decreasing from 70.5% to 67.7%. In turn, USDC marked a similar margin of growth to USDT’s decline, registering an increase in market share from 18.4% to 21.5%. This increase in USDC market share partly occurred due to its status as a more preferred stablecoin for decentralized finance (DeFi). In 2024, the total value locked (TVL) across the DeFi sector has nearly doubled, fueling heightened demand for USDC.

As for lower-cap stablecoins, Ethena’s USDe emerged as a standout performer, with its market share skyrocketing by over 40 times to 2.88%, securing its position as the third-largest stablecoin by the end of 2024.

Chart: Total Supply Distribution by Stablecoin

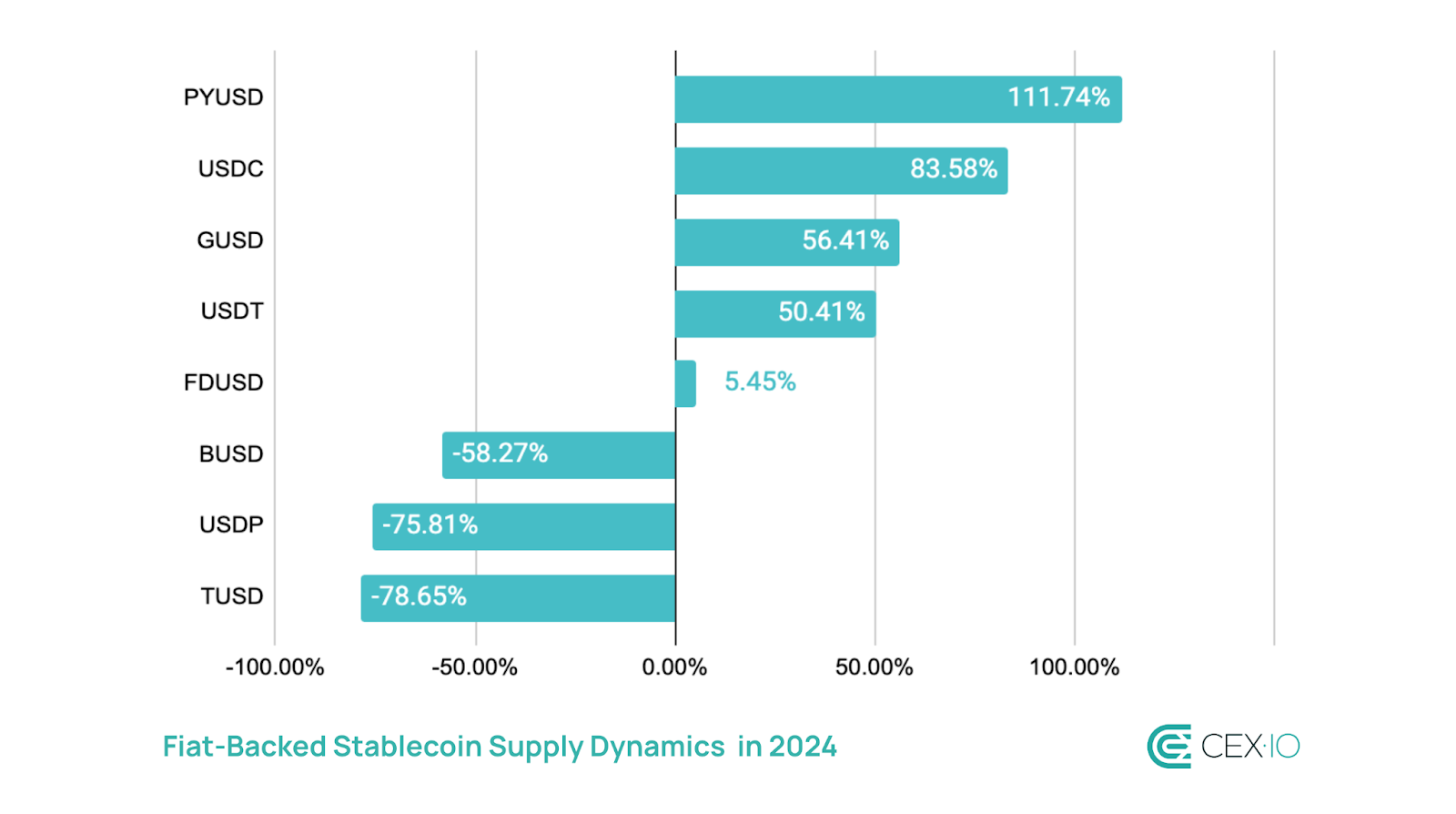

Fiat-Backed Stablecoins

Fiat-backed stablecoins maintained their dominance, but experienced nuanced shifts. The total supply of fiat-backed stablecoins grew by 54.8% in 2024, although their weight in the overall stablecoin market cap decreased from 93.62% to 92.2%. The major catalyst behind this drop was the rising adoption of yield-bearing stablecoins, which primarily utilize crypto-backed collateral and/or algorithmic peg preservation mechanisms.

PYUSD emerged as the leader in supply growth within this category in 2024, primarily due to its expansion to the Solana network mid-year. Solana even temporarily became the largest host of PYUSD, but then supply distribution shifted toward Ethereum.

TUSD saw the steepest decline, with its market cap contracting by over 78%, as the asset lost its top use case following an exclusion from Binance’s launchpool. The TUSD depeg and regulatory issues further escalated the stablecoin drop.

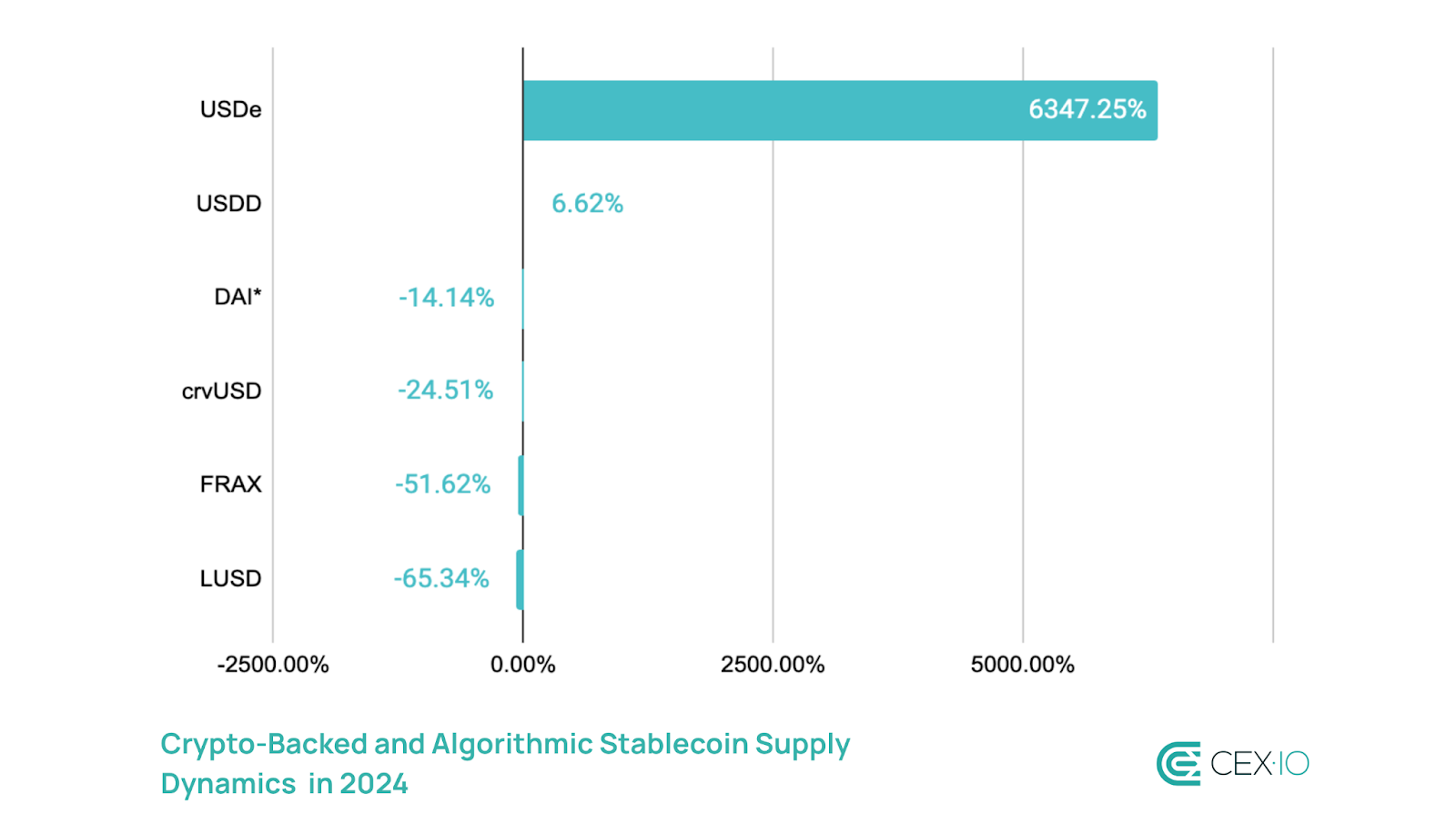

Crypto-Backed and Algorithmic Stablecoins

This category saw explosive growth in 2024, with its total supply increasing by 92%. However, this increase was primarily due to Ethena’s USDe emerging as a transformative force and registering a supply increase of over 6,300%, despite its controversial debut. USDe supply significantly ramped up in Q4, amid rising adoption of Ethereum-based stablecoins and the launch of staked USDe (sUSDe) on Aave. This helped the asset overtake DAI as the largest stablecoin in this category by December, now accounting for a 37% share of the sector.&

Dai experienced a supply reduction due to the launch of USDS in September, its upgraded version that absorbed over $1 billion of DAI’s supply by the end of 2024. However, when combined, DAI and USDS supply reflected a 10% increase compared to DAI’s supply at the start of 2024.

*Dai performance exclude DAI upgraded to USDS

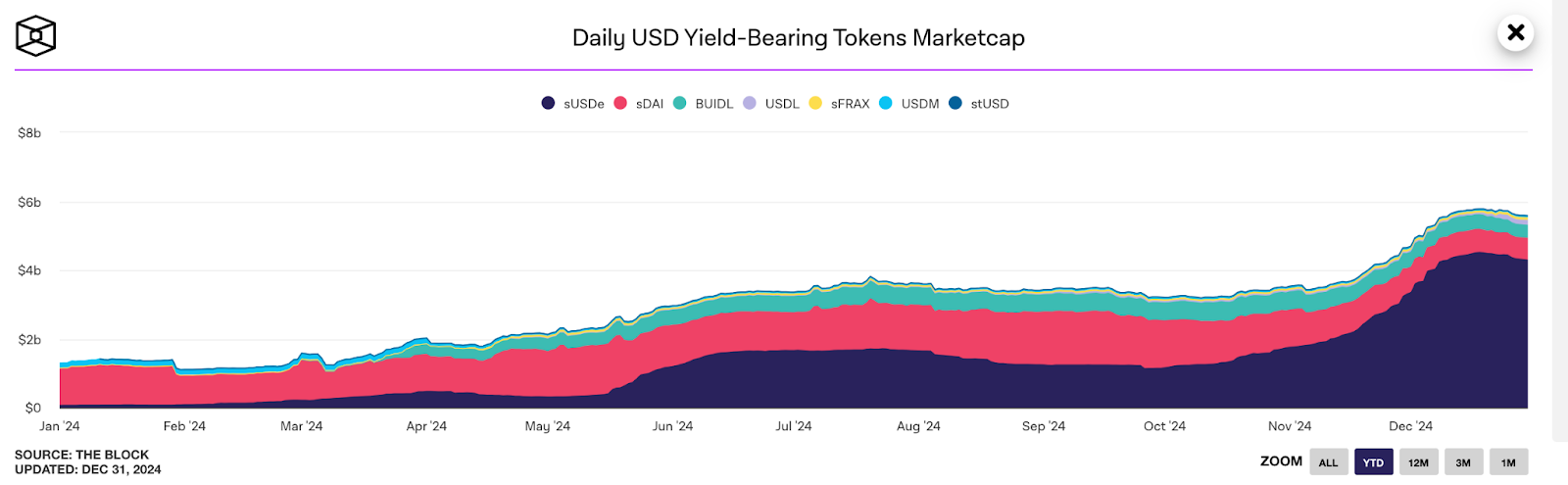

Yield-Bearing Stablecoins

Yield-bearing stablecoins emerged as one of the hottest segments in this space, with its combined market cap surging by over 583% in 2024. This jump was primarily due to adoption of sUSDe, which became the dominant force in this sector, with its market cap increasing by more than 5,800% in a year.&

As such, the weight of yield-bearing stablecoins tripled in a year, now accounting for nearly 3% of the total stablecoin market. Notably, they gained traction despite facing a tightening regulatory environment. At the end of 2023 a U.S. court ruled that stablecoins in combination with related yield protocols such as Terra’s UST are securities.

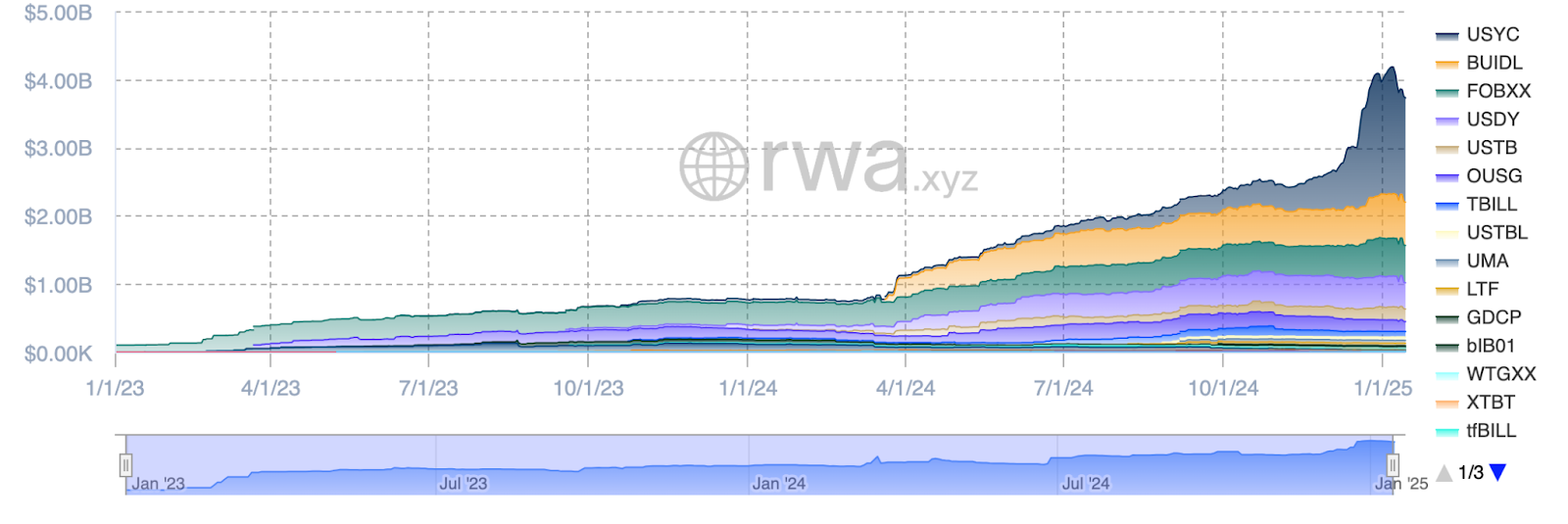

While sUSDe adopts a “delta-neutral” trading strategy involving long and short positions to generate yield, the wider yield-bearing stablecoin segment followed a different route focused on real-world assets (RWA), especially U.S. Treasuries. The sector of tokenized treasuries surged by over 414% last year, primarily due to the adoption of newly launched yield-bearning stablecoins and RWA projects, including BlackRock’s BUIDL, Paxos’ USDL, Mountain Protocol’s USDM, and Usual Money’s USD0.&

USD0 showed the largest surge among RWA-focused stablecoins, reaching a market cap of $1.7 billion and achieving a 39-fold increase in supply since its inception in June 2024. Due to USD0’s rapid growth, USYC, which serves as a primary backing asset for USD0, became the largest holder of tokenized U.S. Treasury bonds, now accounting for over 40% of the market.

Chart: U.S. Treasury Market Cap Among RWA Projects

Supply by Network

General Distribution

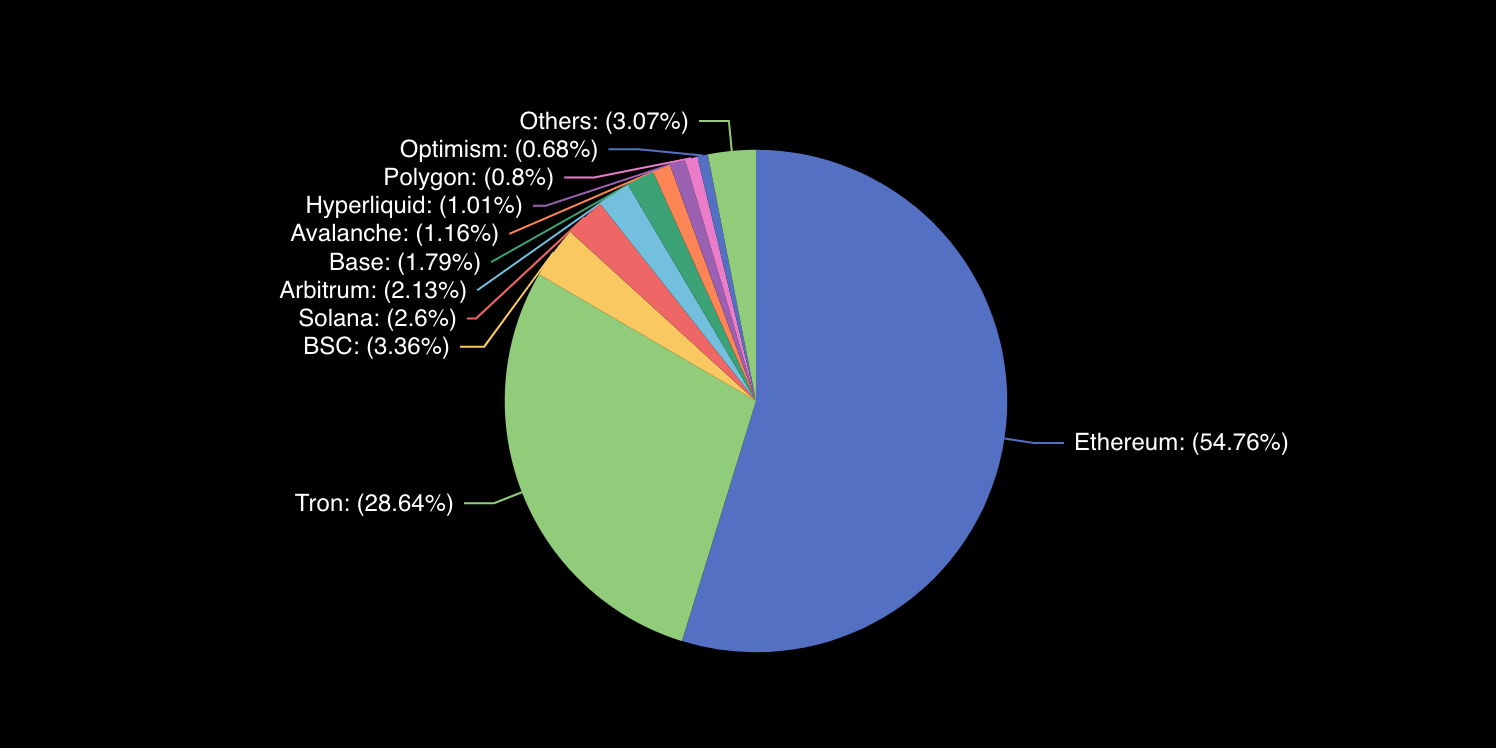

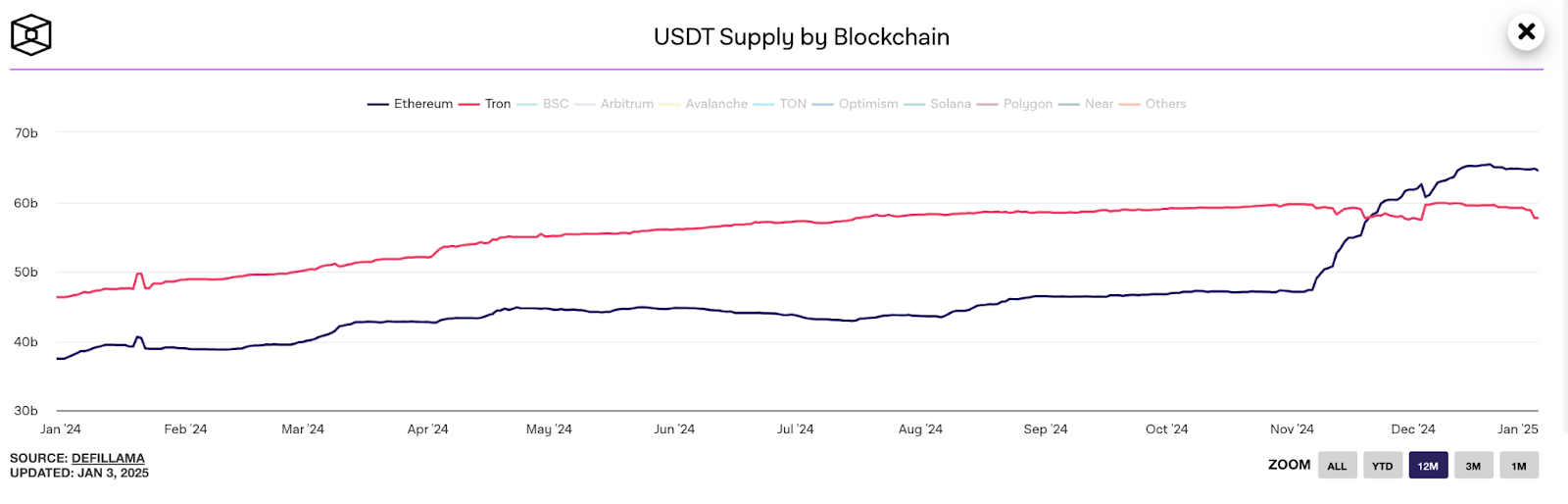

Ethereum and Tron continued to dominate as the primary networks hosting stablecoins, together accounting for over 83% of the market by the end of 2024. However, their combined share fell from 90% at the beginning of the year, highlighting the ongoing diversification of stablecoin adoption across other networks, particularly to Solana, Arbitrum, Base, and Aptos. This shift was particularly pronounced for Tron, which saw its market share decline significantly from 38% to 29%.

Chart: Stablecoin Market Cap Distribution by Network

Dominant Networks

Ethereum’s stablecoin market cap grew by 65% in 2024, reaching a new all-time high. This growth was partly driven by a significant reduction in transaction fees following the Dencun upgrade in March, which enhanced Ethereum’s competitiveness as a stablecoin hub. In turn, post-election optimism surrounding the development of the DeFi space under the new U.S. administration provided further momentum for Ethereum’s stablecoin supply expansion.&

Within the Ethereum network, USDT strengthened its dominance, increasing its share from 55% to 62%, while USDC’s share decreased from 29% to 25%. This shift primarily occurred amid Tether’s aggressive minting in Q4 and supply redistribution from other networks, primarily Tron, to satisfy increased demand.

As a result, the surge in USDT supply was so substantial that Ethereum reclaimed its position as the largest network hosting USDT. This transition is particularly important as USDT accounts for over 98% of the entire stablecoin supply on the Tron network.&

Compared to Ethereum, Tron experienced slower growth, with its stablecoin market cap increasing by only 19% in 2024. This is because Ethereum’s reduced transaction fees partly undercut Tron’s traditional cost-efficiency advantage. Moreover, Tron’s stagnant DeFi ecosystem, evidenced by an 8% decline in TVL during the year, further limited its growth potential.

Chart: Tron’s Stablecoin and TVL Dynamics in 2024

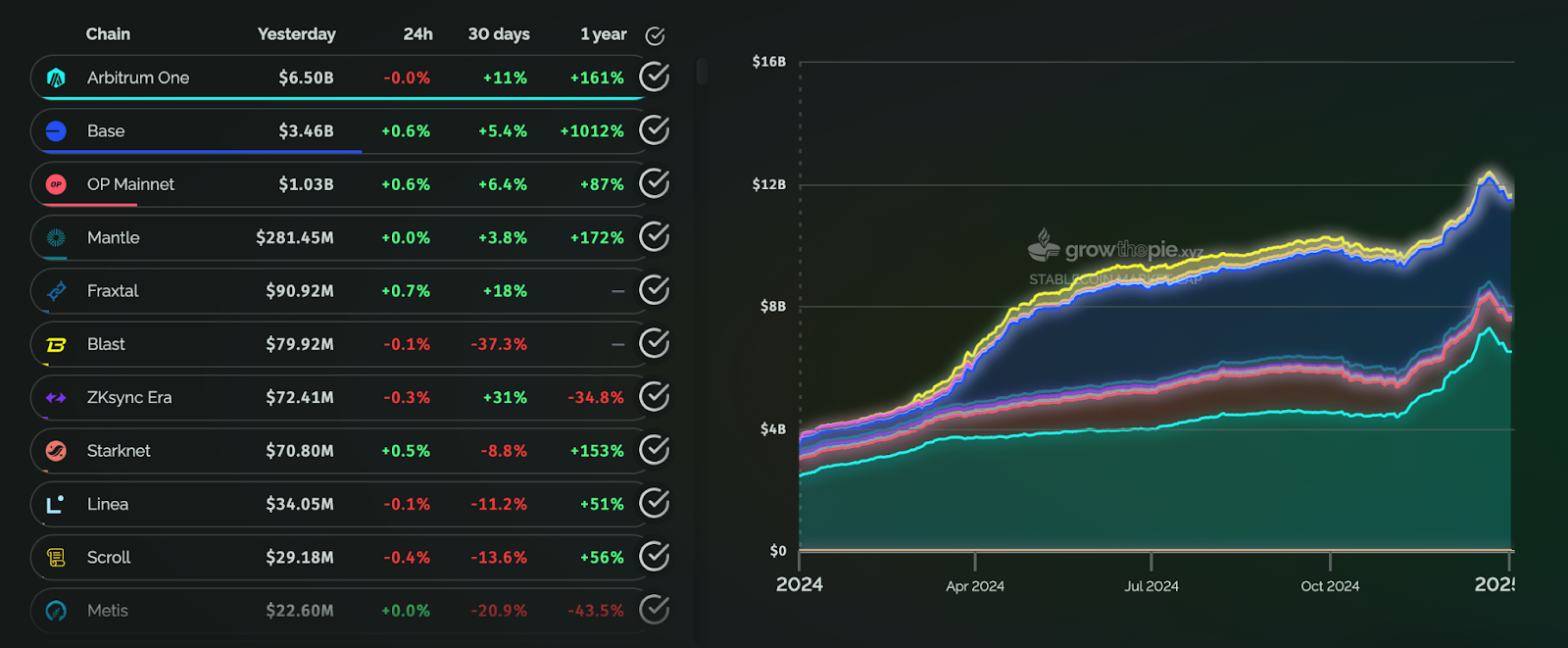

L2 Networks

Ethereum’s Layer-2 (L2) networks became significant beneficiaries of stablecoin expansion in 2024, with their combined stablecoin market cap growing by over 218%. The Dencun upgrade played a key role by drastically reducing transaction fees on L2 networks, with some protocols experiencing cost reductions of up to 99%. This made L2 networks increasingly attractive to Ethereum users to conduct transactions and utilize decentralized applications (dApps).

Among these networks, Arbitrum remained the one with the largest stablecoin supply. However, its share in total L2 stablecoin supply decreased from 65% to 55% due to the rapid rise of Base and the launch of new L2 networks. Base, in particular, saw substantial growth starting in March, fueled by memecoin hype and accelerated DeFi development within the network. Other catalysts included Coinbase’s transition of customer USDC balance to Base, as well the introduction of gasless transactions on Base.&

Chart: L2 Stablecoin Market Cap Dynamics in 2024

Other Networks

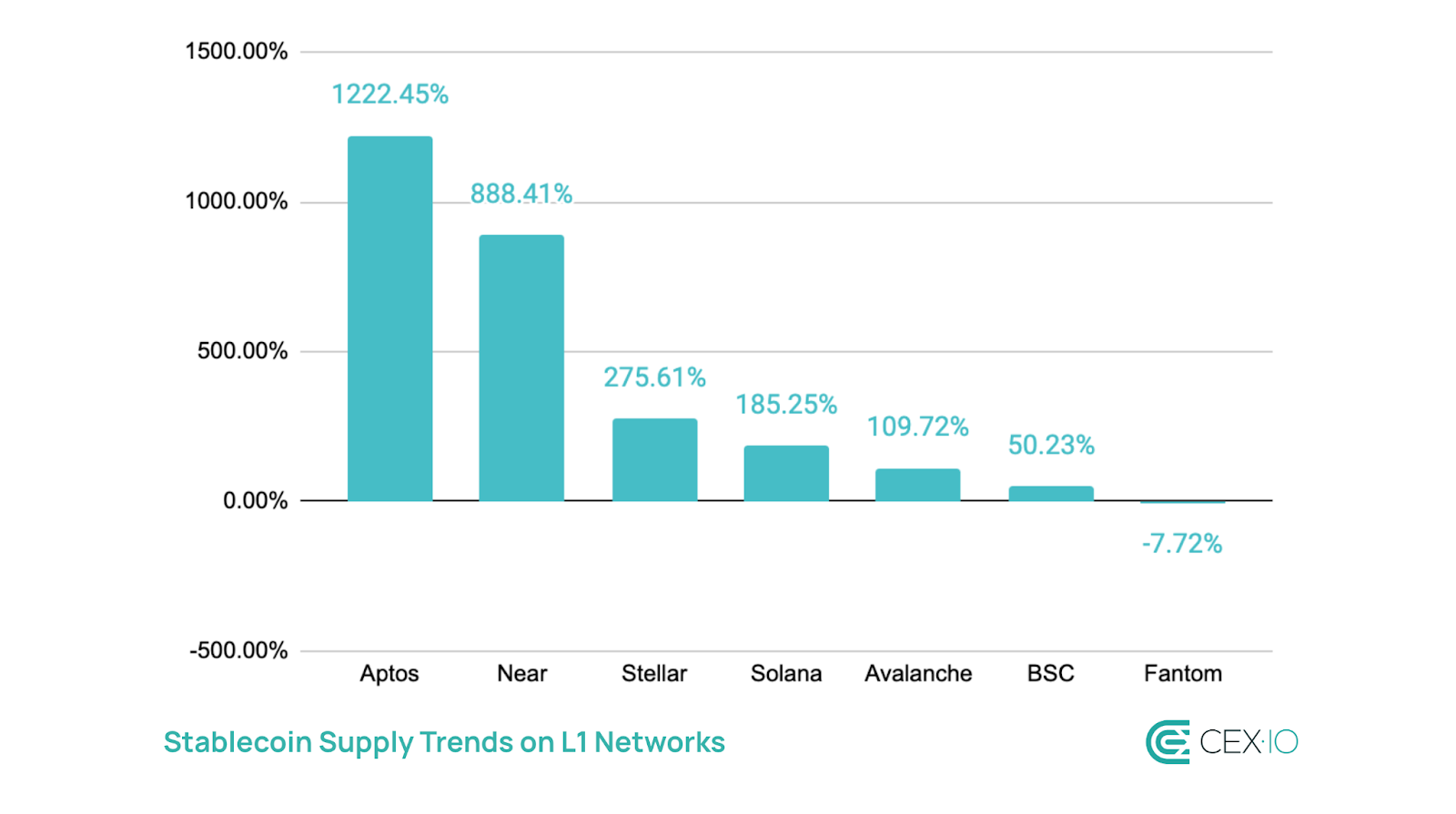

Among L1 networks hosting over $100 million in stablecoins, Aptos turned out a standout performer with a four-digit percentage increase in hosted stablecoin market cap. This growth was primarily driven by a massive increase of USDT supply, especially in the fourth quarter. At the start of 2024, USDT represented only 24% of Aptos’ stablecoin supply, but by year’s end, its share had surged to 70%, displacing USDC’s dominance within the network.

In contrast, Solana saw its stablecoin growth primarily driven by USDC, whose share rose from 53% to 74%. This increase aligned with Solana’s overall ecosystem growth, as stablecoins on the network were predominantly used for DeFi and other dApp activities.&

Meanwhile, TON emerged as a notable newcomer in stablecoin adoption. Its stablecoin market cap surged to $1.2 billion following the adoption of USDT in June, with USDT remaining the only stablecoin on the network.

Transaction Volume

Total Transaction Volume

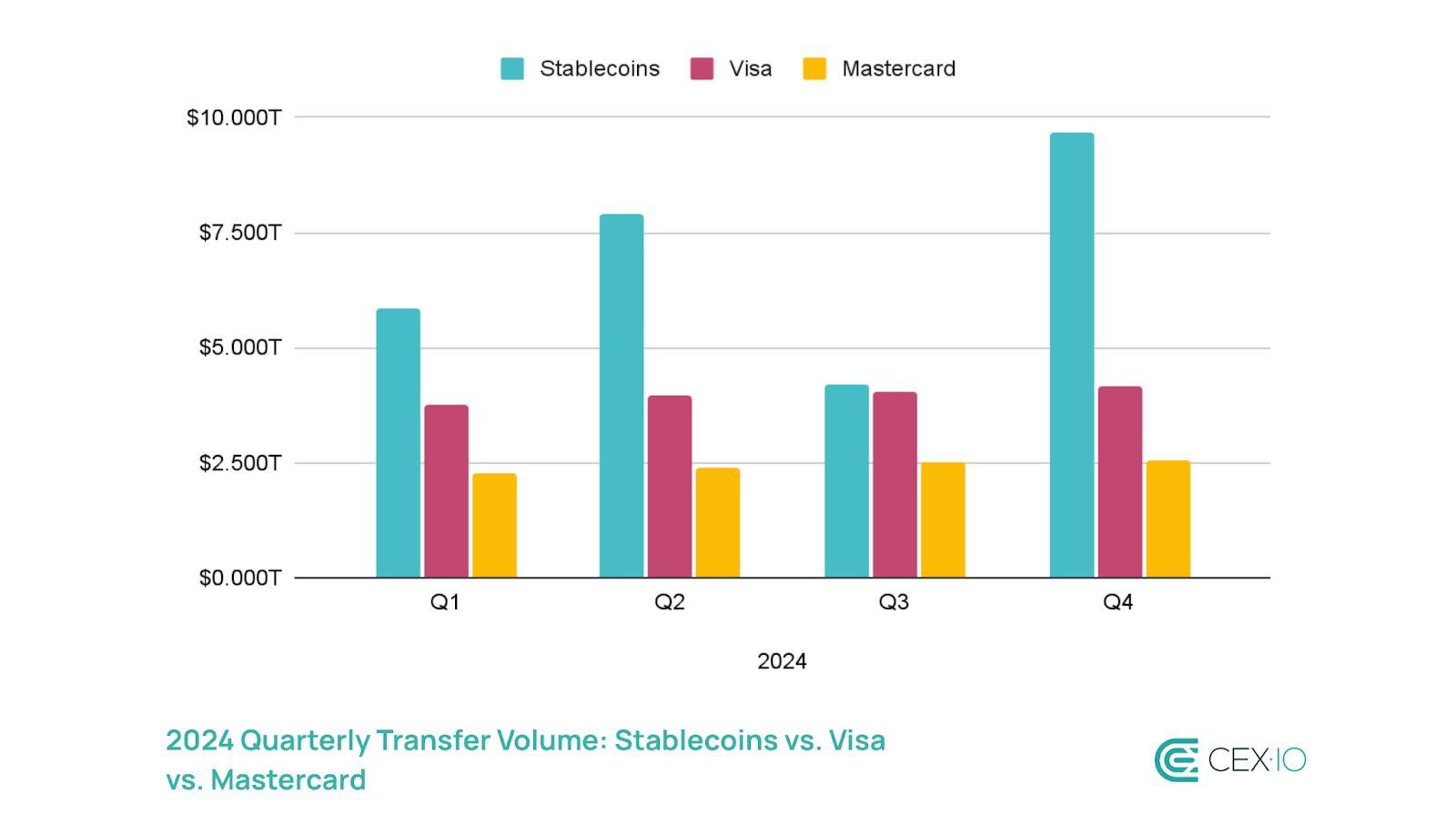

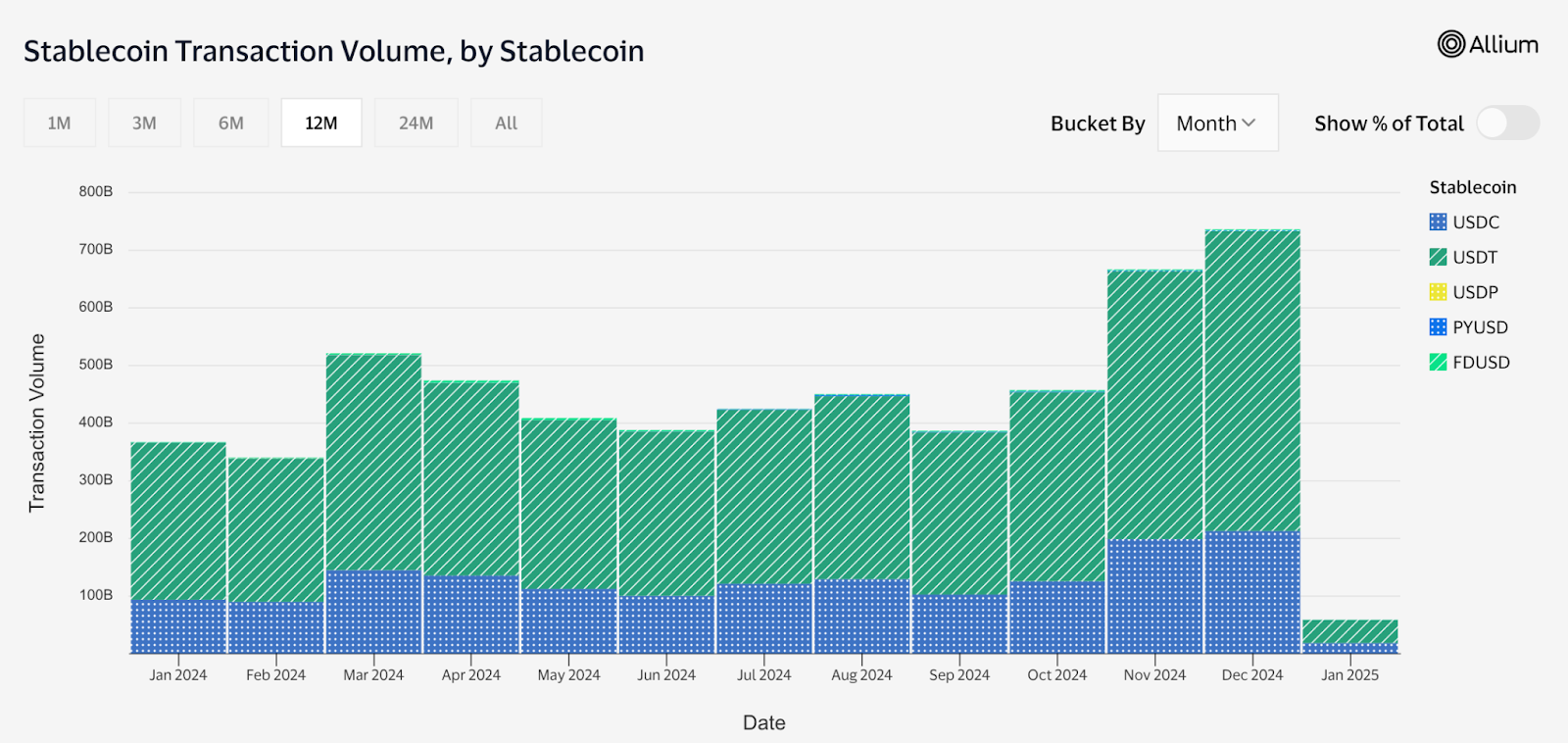

In 2024, total stablecoin transfer reached $27.6 trillion, surpassing a combined transaction volume of Visa and Mastercard over the same period by 7.68%. Notably, stablecoins have been exceeding traditional payment providers throughout the entire year, despite a significant drop in Q3 amid decreased activity on the wider crypto market.

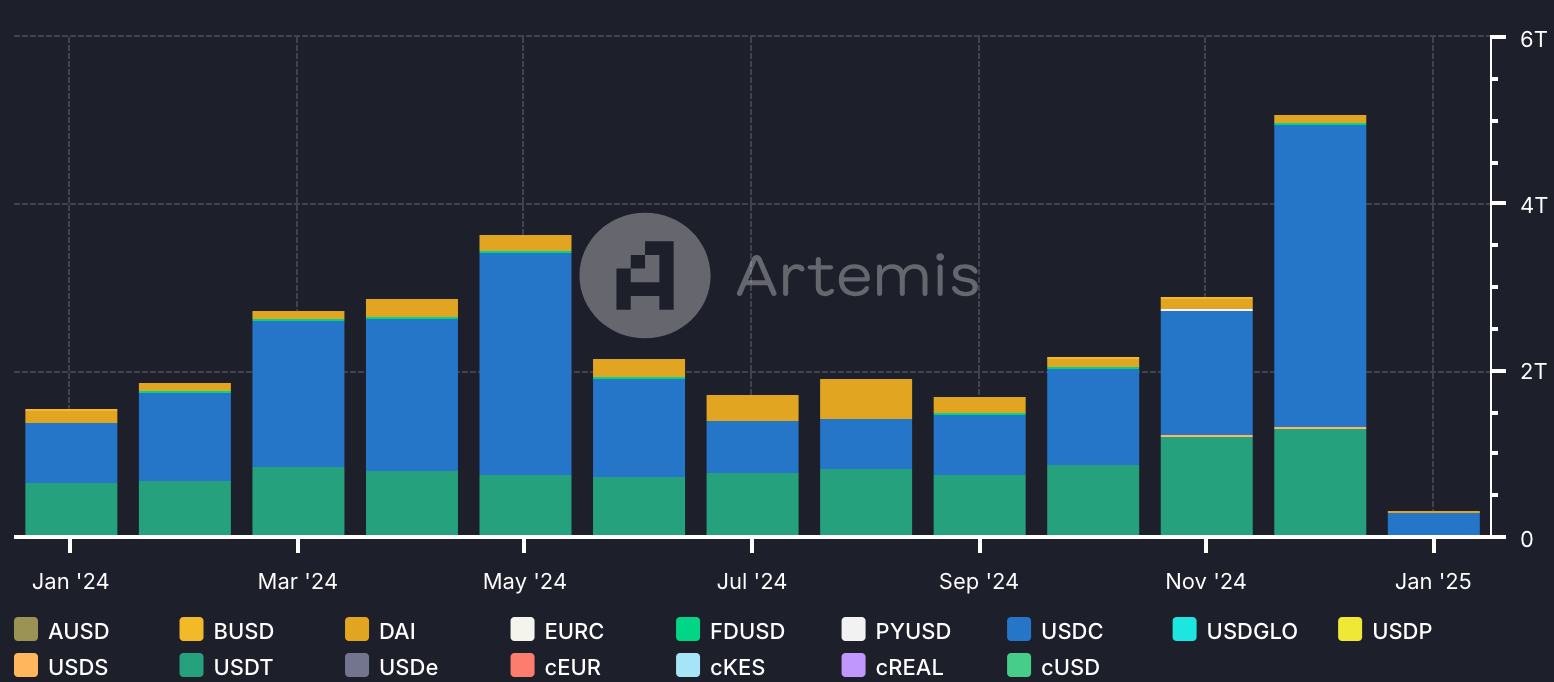

USDC reinforced its position as the preferred stablecoin for on-chain activity, accounting for 70% of the total combined transfer volume. Despite dominating raw transaction volume throughout the year, USDC’s influence waned slightly in Q3 due to a temporary decline in dApp activity. USDT also saw a substantial rise, with its total transfer volume more than doubling; however, its market share fell from 43% to 25%.

Chart: Total Transfer Volume by Stablecoin

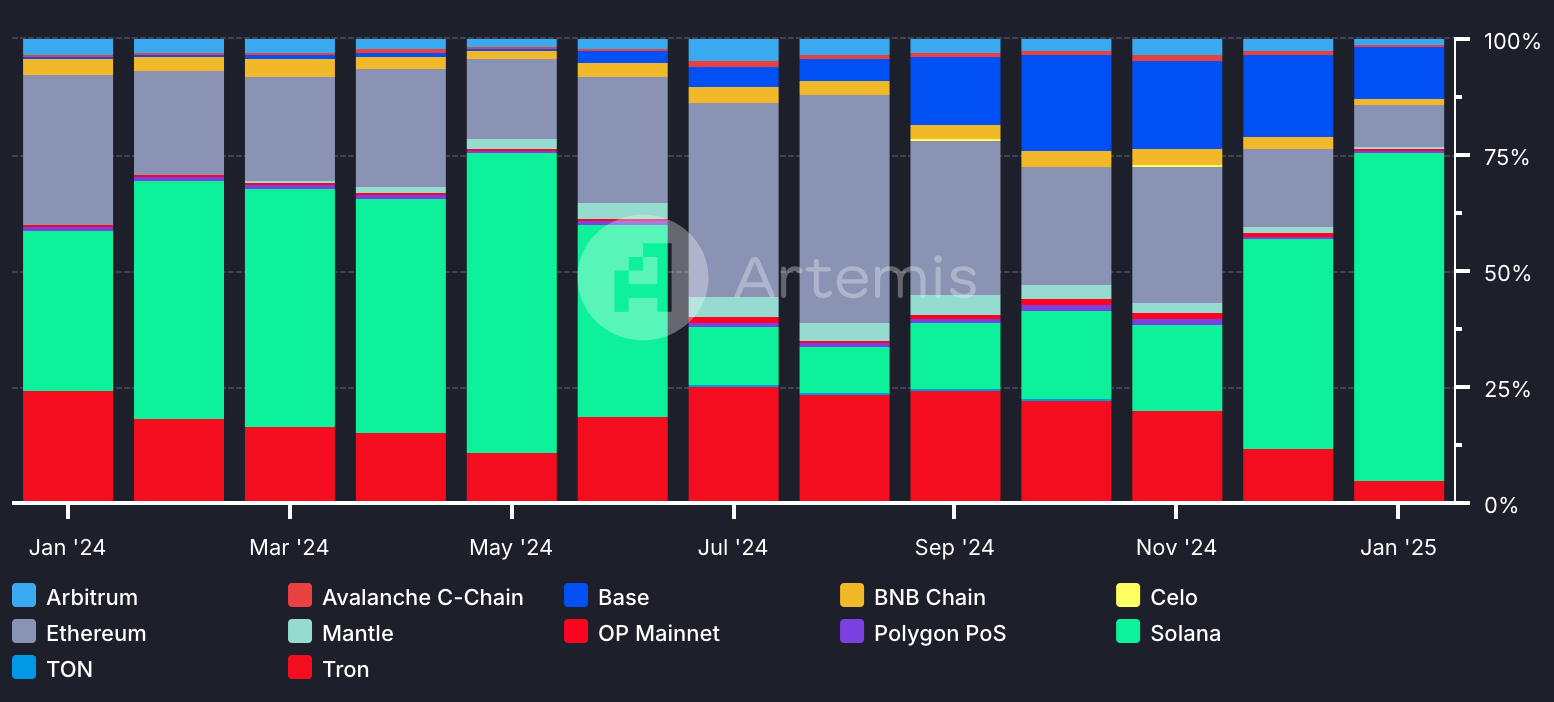

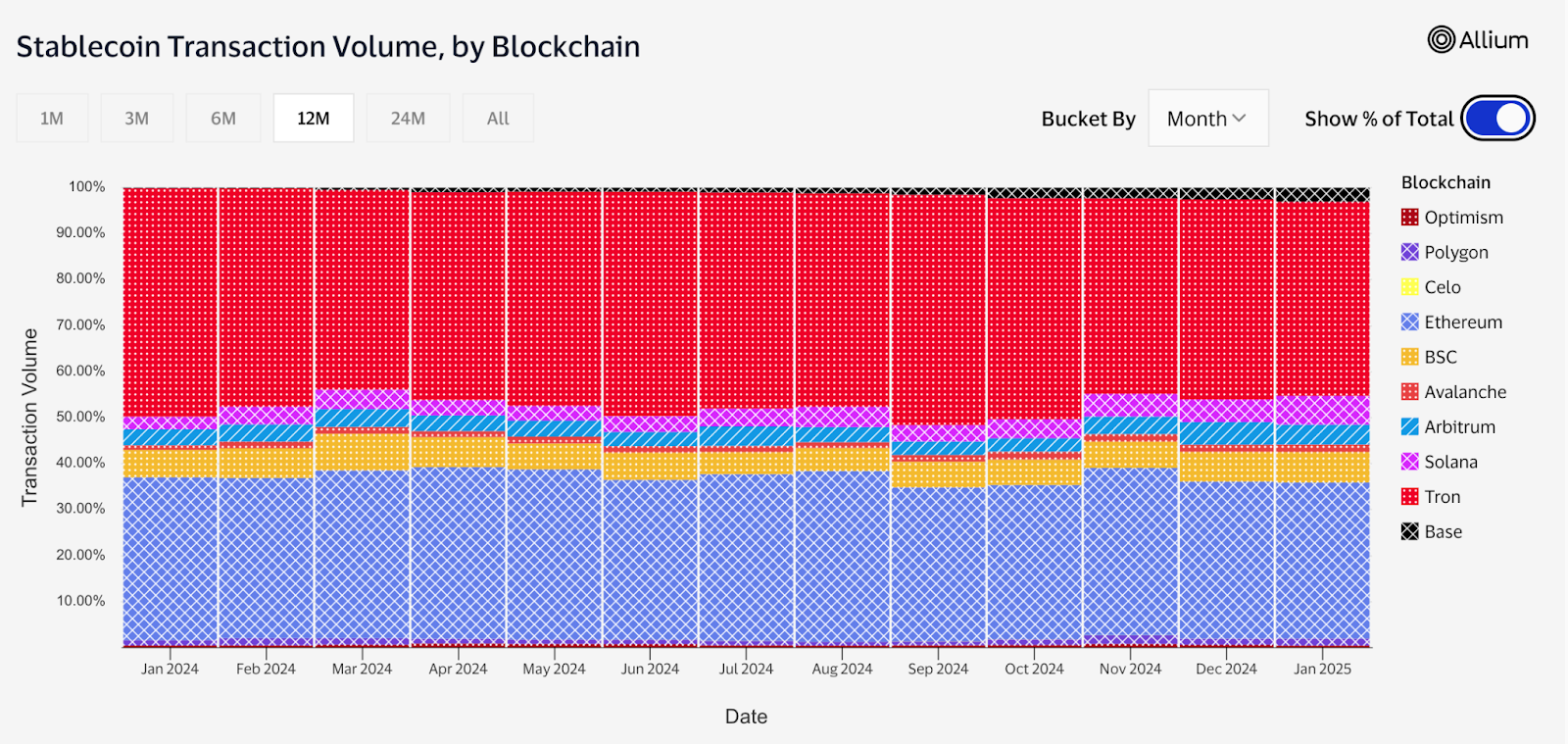

Starting in January 2024, Solana surpassed both Tron and Ethereum to become the most active network for stablecoin operations. This surge in activity positioned Solana as the primary driver of USDC’s market share growth, with total USDC transactions strongly correlated to Solana-based activity. USDC accounts for over 73% of Solana’s stablecoin supply.&

Chart: Total Stablecoin Transfer Volume Distribution by Network

Adjusted vs. Unadjusted Transaction Volume

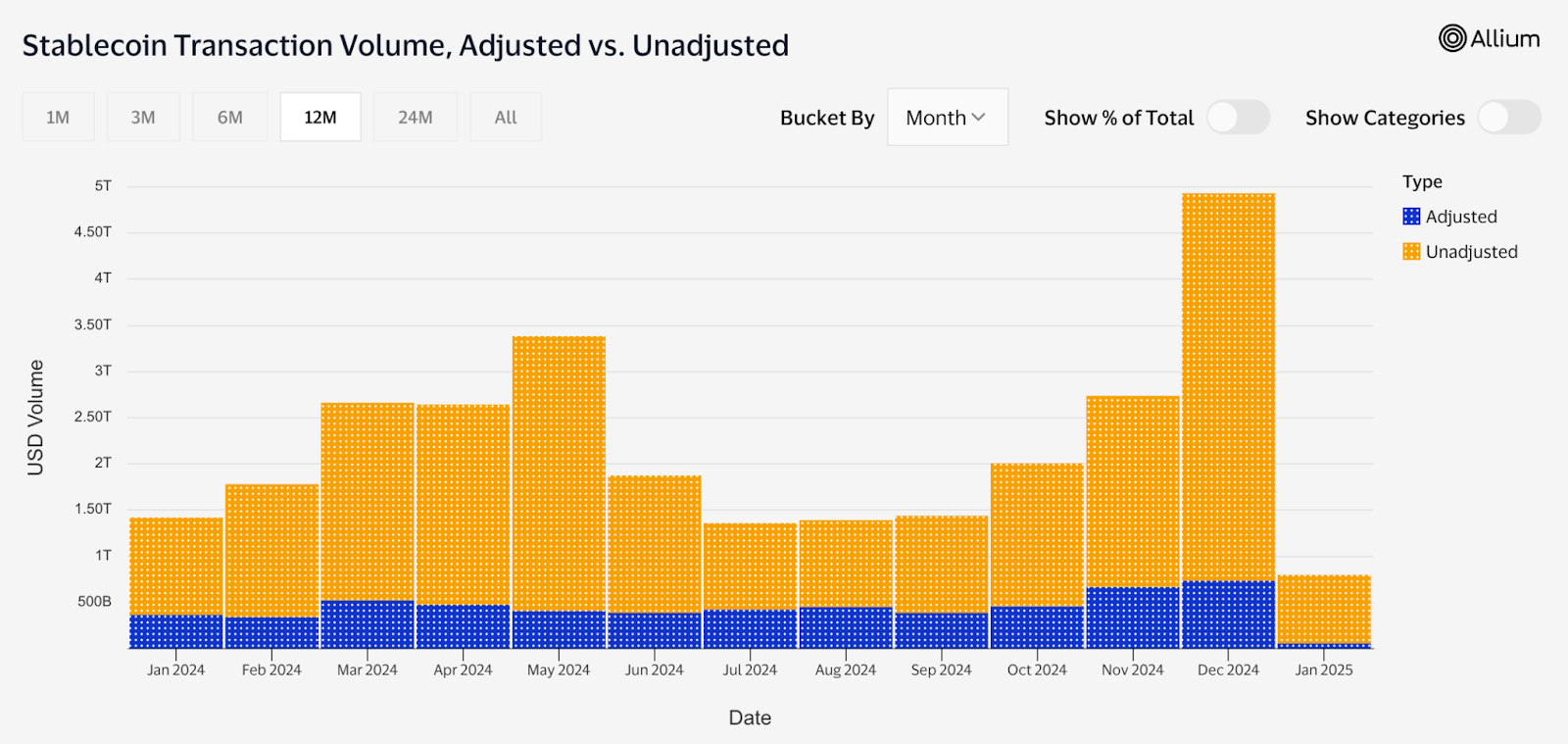

Now let’s distinguish between total and adjusted volume that excludes bot activity, internal smart contract transactions, and internal exchange transfers. On average, 77% of 2024’s total stablecoin transaction volume fell into the unadjusted category, largely driven by bot transactions. The bot activity experienced a fourfold increase compared to 2023, increasing its share from 80% to 90% in the unadjusted category. This means that 70% of stablecoin transaction volume in 2024 was related to bot transfers.

USDC dominated the unadjusted category, making up over 65% of the volume. This underscores the fact that much of USDC’s transaction activity was driven by bots.

Chart: Unadjusted Transaction Volume by Stablecoin

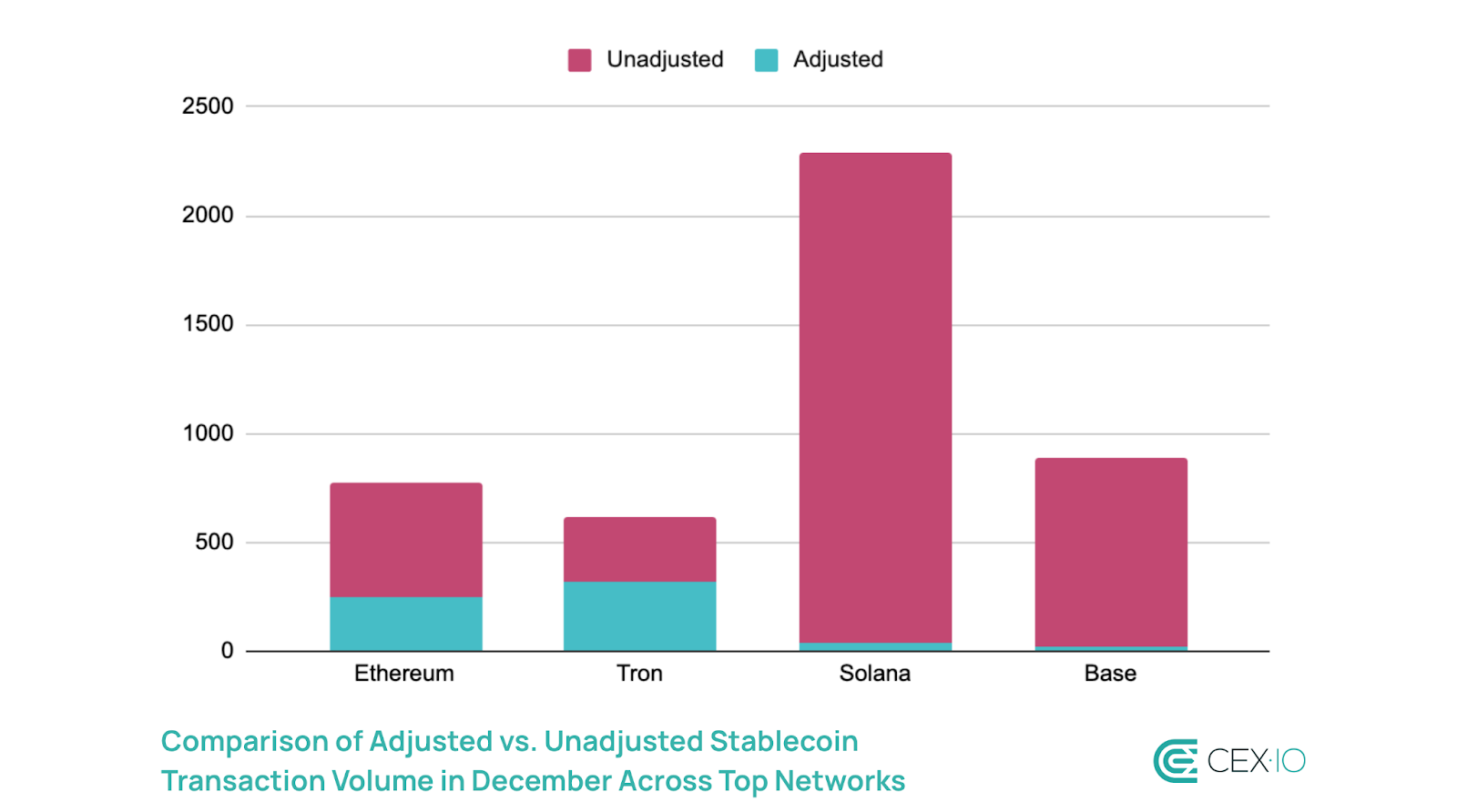

Networks such as Solana and Base, where USDC supply dominates, saw unadjusted transactions represent over 98% of stablecoin activity as of December 2024. Due to the bot activity, Base even managed to surpass Ethereum in total stablecoin transaction volume in Q4 2024.&

Aside from general attributes like high transaction speed and low transaction costs that are essential for a productive bot environment, the rapidly rising DeFi ecosystem and the frequent launch of meme tokens provided fertile ground for bots on Solana and Base. For instance, in December, memecoins accounted for over 56% of DEX trading volume on Solana.

However, it’s important to point out that high bot activity within the network doesn’t necessarily mean “worse” transfer volume. While bots can be used for harmful practices like frontrunning, sandwich attacks, pump and dump schemes, and snipping liquidity pools, they also improve market efficiency through arbitrage. In addition, bots are used by paymasters to cover gas fees on behalf of users, smart contracts to execute recurring transactions, and aggregators to deliver deeper liquidity. As a result, bot dominance in stablecoin transactions could also represent the maturation of certain networks.

Adjusted Transaction Volume

If removing the bot activity from the equation and focusing on adjusted volume, which captures transfers to centralized exchanges (CEXs), decentralized exchanges (DEXs), and DeFi operations, the stablecoin transaction landscape will be completely different. Adjusted stablecoin transfer volume doubled in 2024, though it still lagged behind the growth of bot-driven activity.&

USDT emerged as the dominant stablecoin for “organic” transactions, accounting for over 68% of adjusted transaction volume. In turn, PYUSD showed the highest adoption growth, tripling its share within adjusted transactions, though it still represented less than 2% of “organic” transaction activity.&

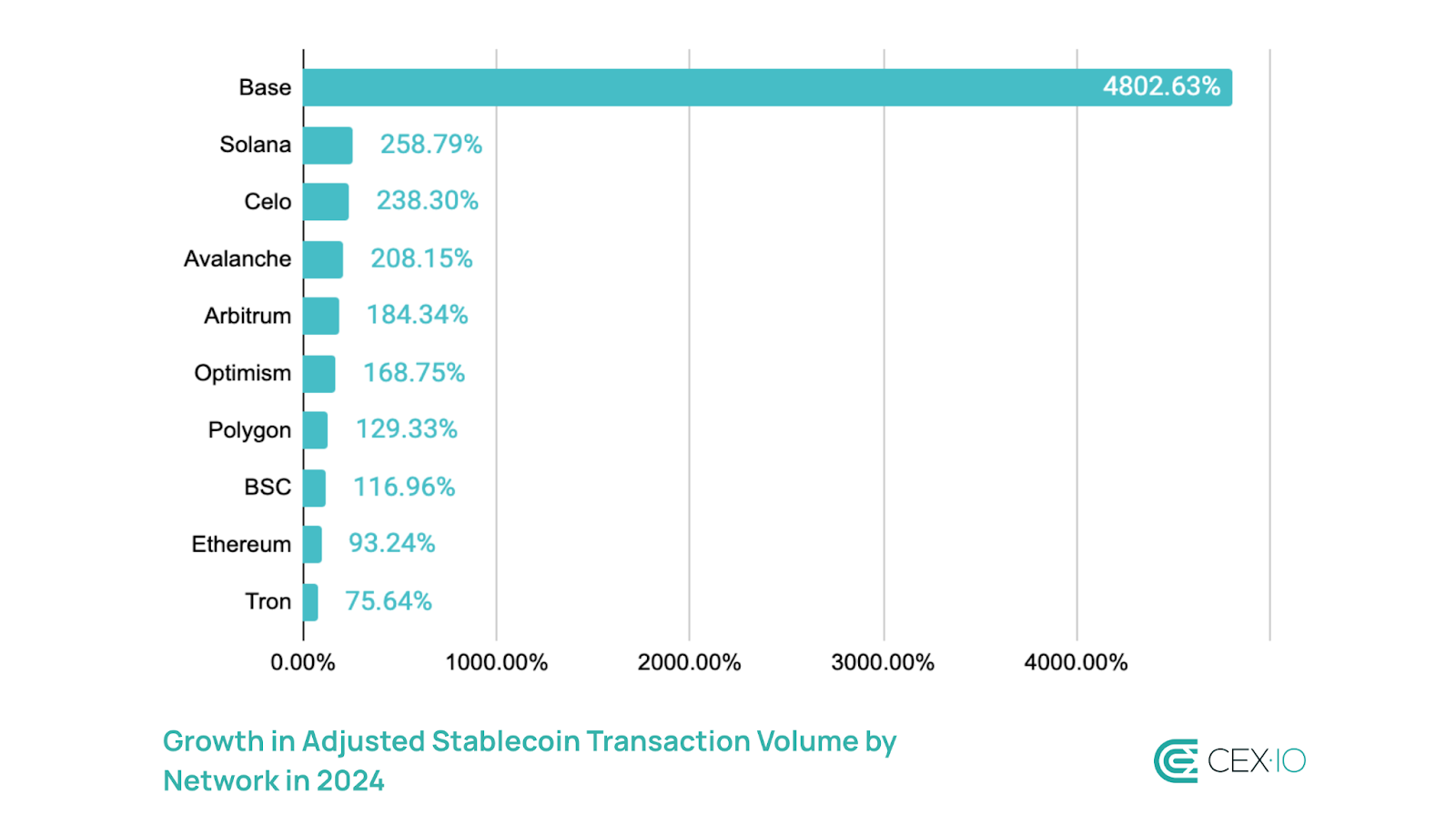

In this category, Tron and Ethereum reclaimed their status as the leading networks for stablecoin transactions. Solana’s share of adjusted volume remained below 5%, despite doubling over the year. Meanwhile, Base experienced rapid growth in the second half of the year, becoming the sixth-largest network for “organic” stablecoin activity.

The rapid rise of Base and the increased presence of smaller networks indicate a broader expansion of stablecoin influence across the industry, with smaller platforms gaining traction for “organic” transaction activities. As such, Base became the best performing network in terms of “organic” growth, experiencing a four-digit increase in 2024.&

Trading Volume

Total Volume

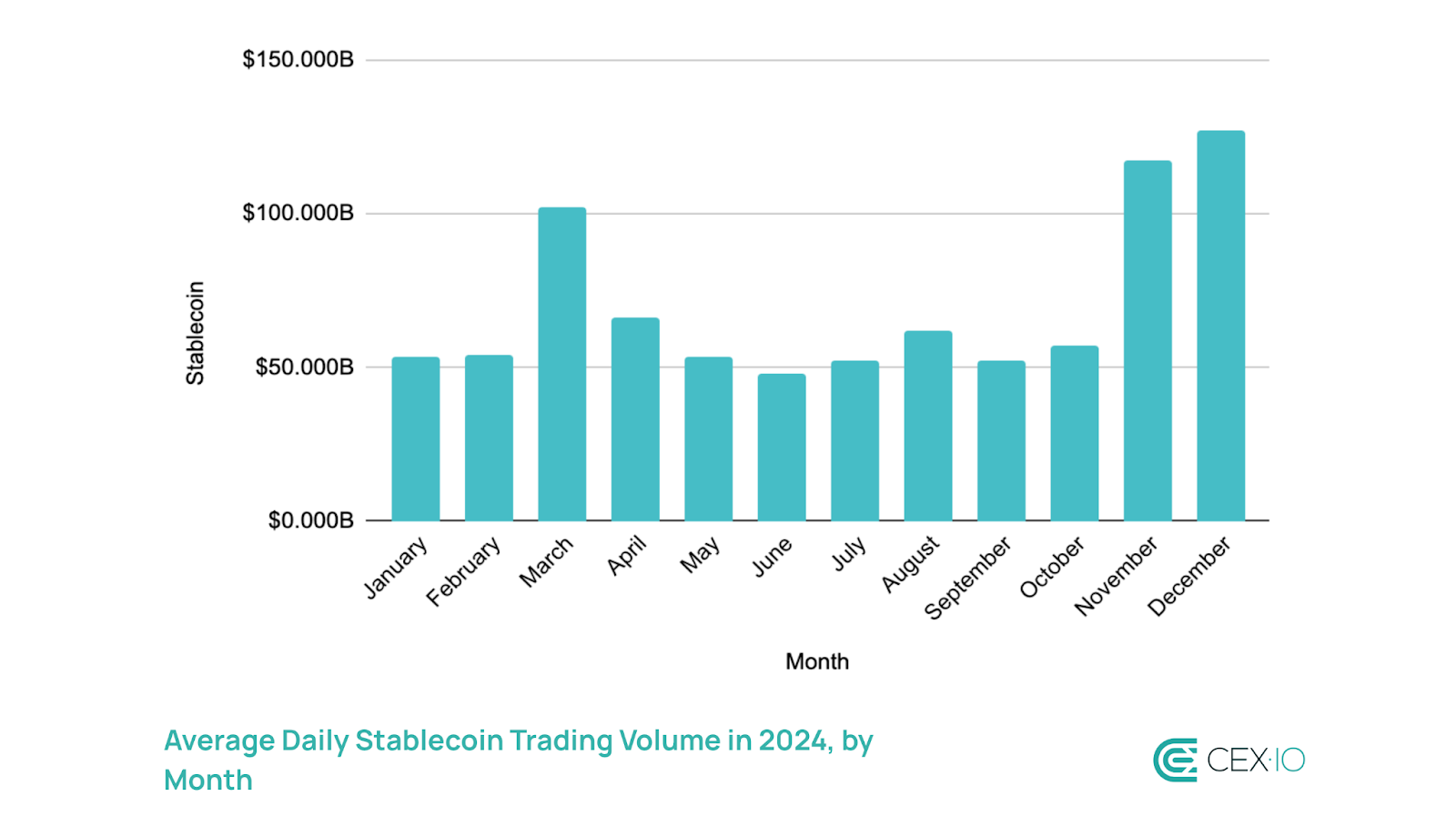

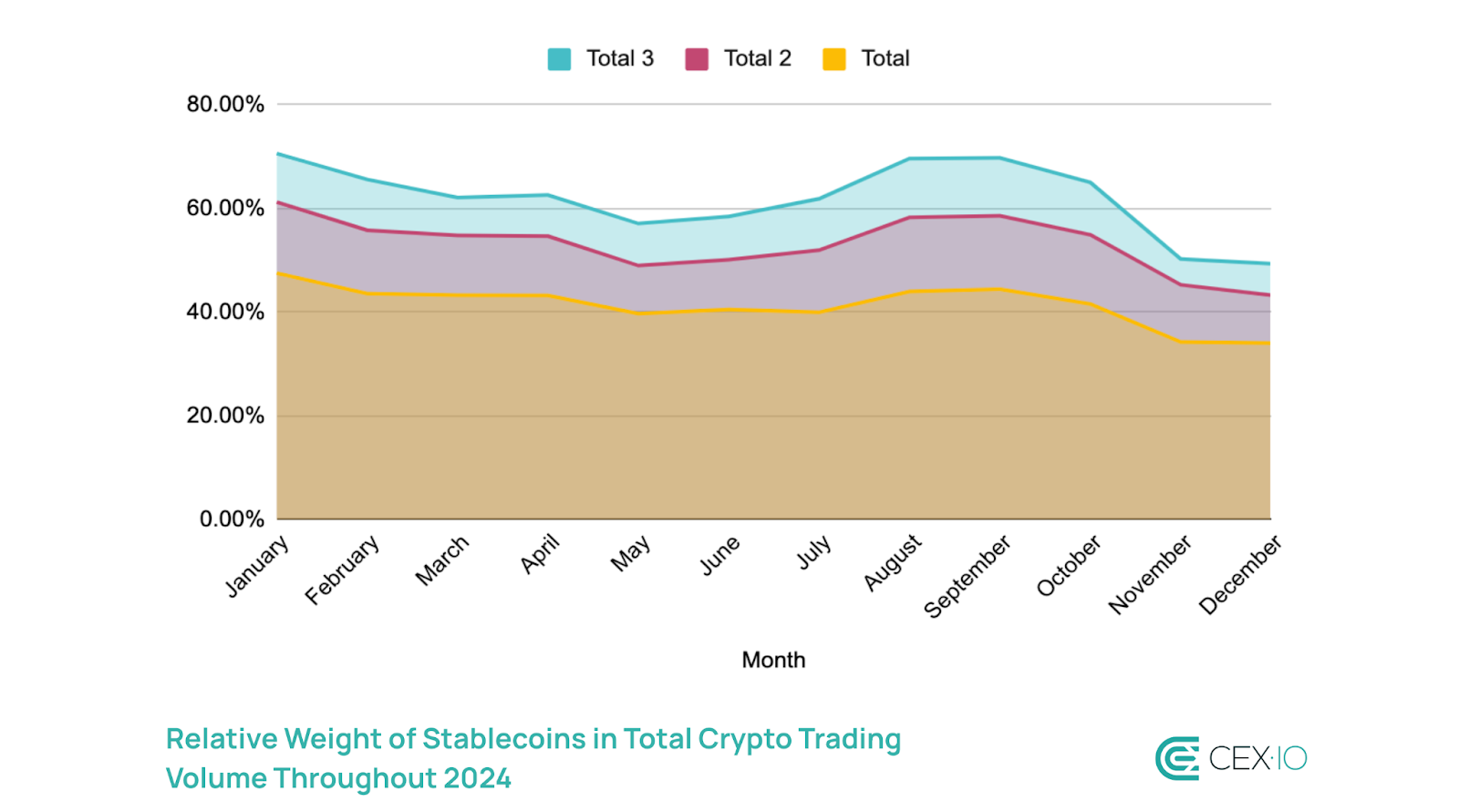

Stablecoins registered over $25.8 trillion in aggregated trading volume in 2024, continuing to gain market share over fiat, and solidifying their position as the preferred medium of exchange on trading platforms. The average daily trading volume among stablecoins soared by over 237% in a year, predominantly as a response to increased activity on wider crypto markets.&

Despite increased trading volume, the weight of stablecoins compared to total crypto trading volume has been in decline throughout 2024. The primary reason was increased adoption of derivative products like perpetual swaps or futures that use cryptocurrencies as collateral, reducing the relative role of stablecoins in total trading volumes. Other catalysts behind decreased weight of stablecoins include rising demand on leverage and expansion of on-chain crypto-to-crypto trading without involving stablecoins, especially among memecoins.

Note: The “Total” value represents overall crypto trading volume, “Total 2” — excludes Bitcoin, while “Total 3” — excludes Bitcoin and Ethereum.

Volume Distribution

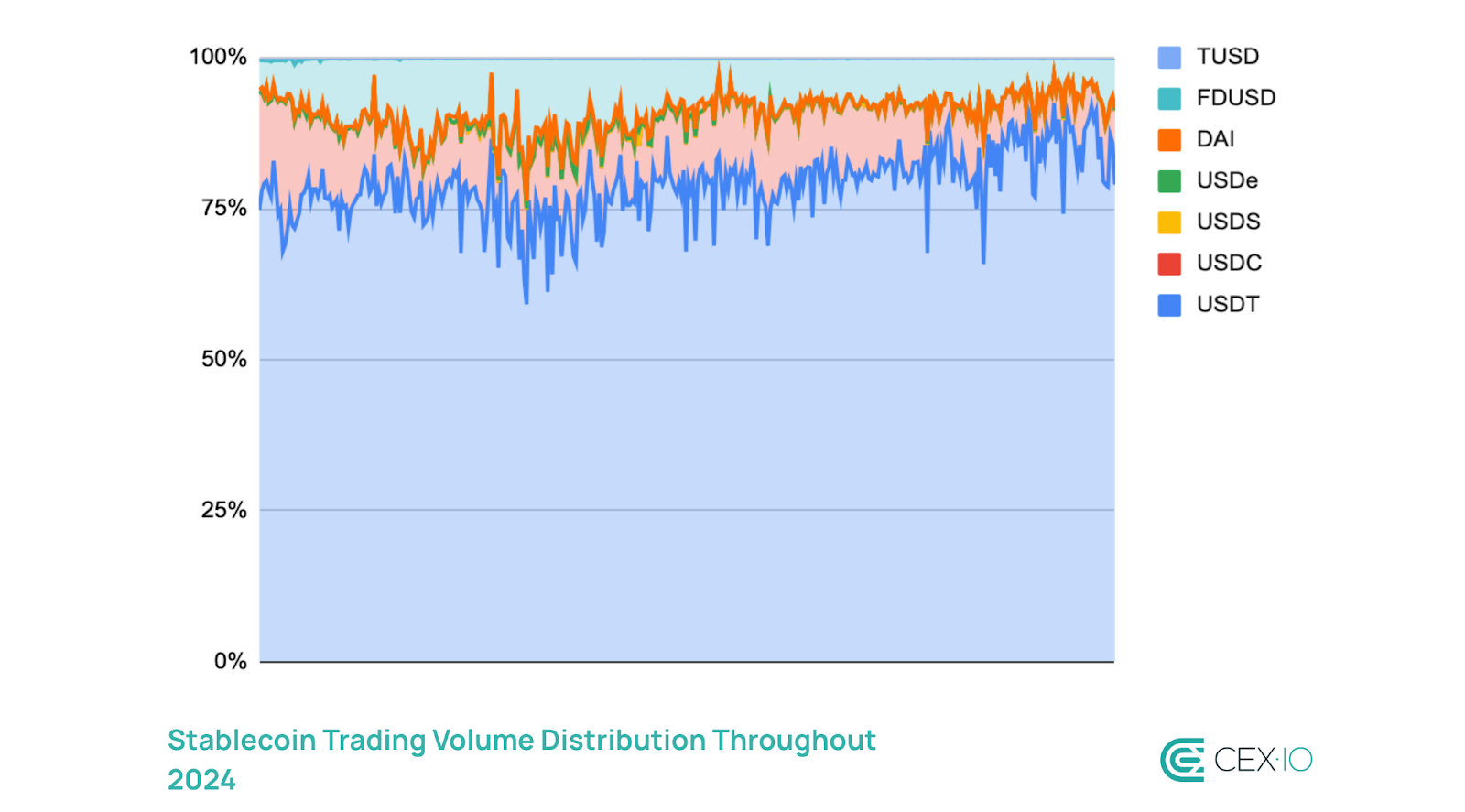

Despite the presence of hundreds of stablecoins, the market remains highly concentrated, with the top six most popular stablecoins contributing to approximately 99% of total trading volume. Among these, USDT maintained its lead as the most favored medium of exchange, accounting for a 79.7% of stablecoin trading volume on average.&

In early 2024, USDT’s market share on CEXs has been trending downwards, declining from 81% to 66%. This decrease can be partly attributed to growing competition from stablecoins like FDUSD and USDC. The former benefited from Binance’s zero-fee promotions, while USDC increase signaled growing presence of regulated alternatives.&

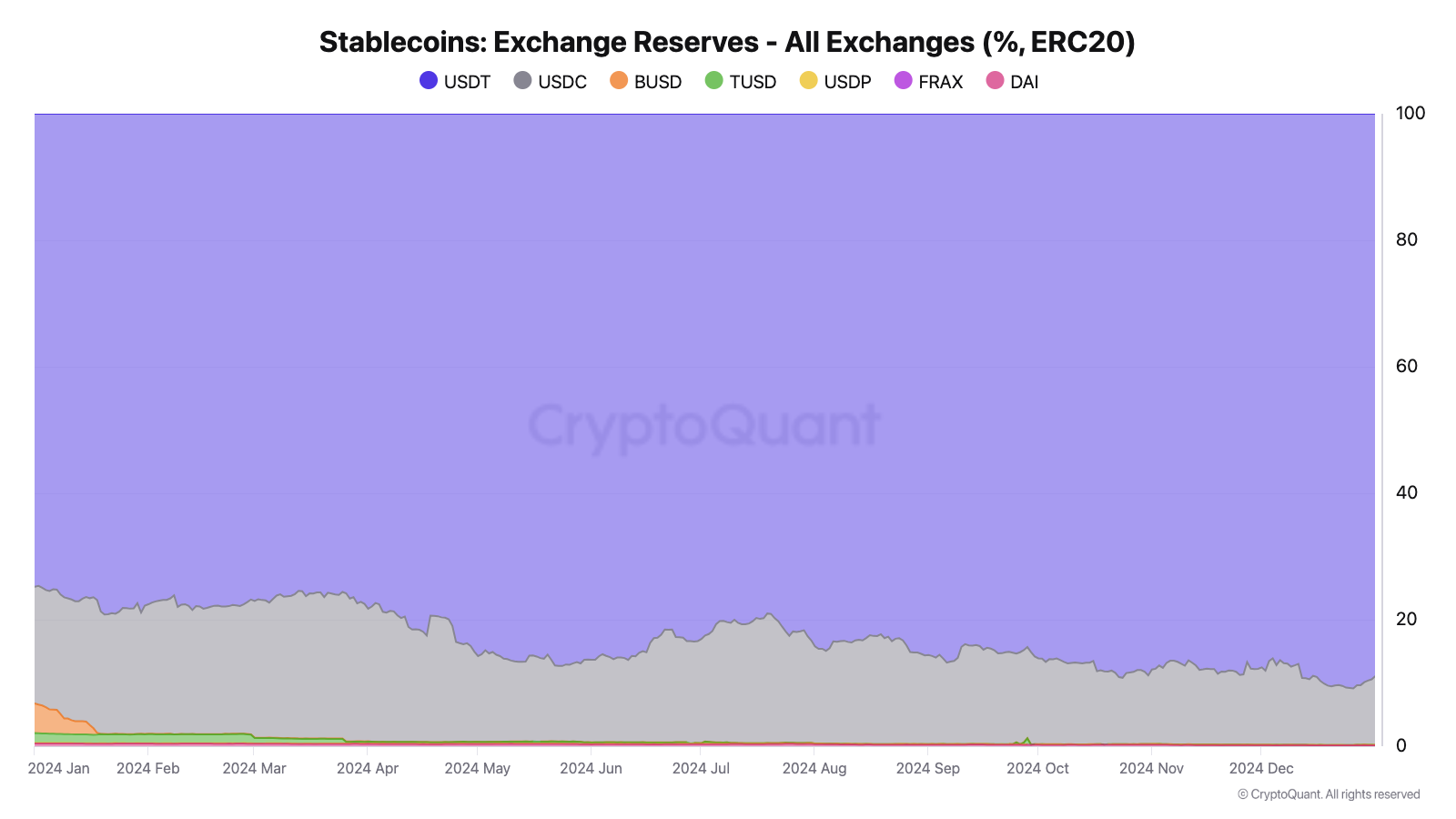

However, in the second half of 2024, USDT dominance in trading volume has been strengthening amid increased exchange reserves. According to CryptoQuant data, exchange reserves of Ethereum-based USDT surged by over 165% in a year, contributing to its share increase from 75% to 90% in total stablecoin exchange reserves.

2025 Outlook&

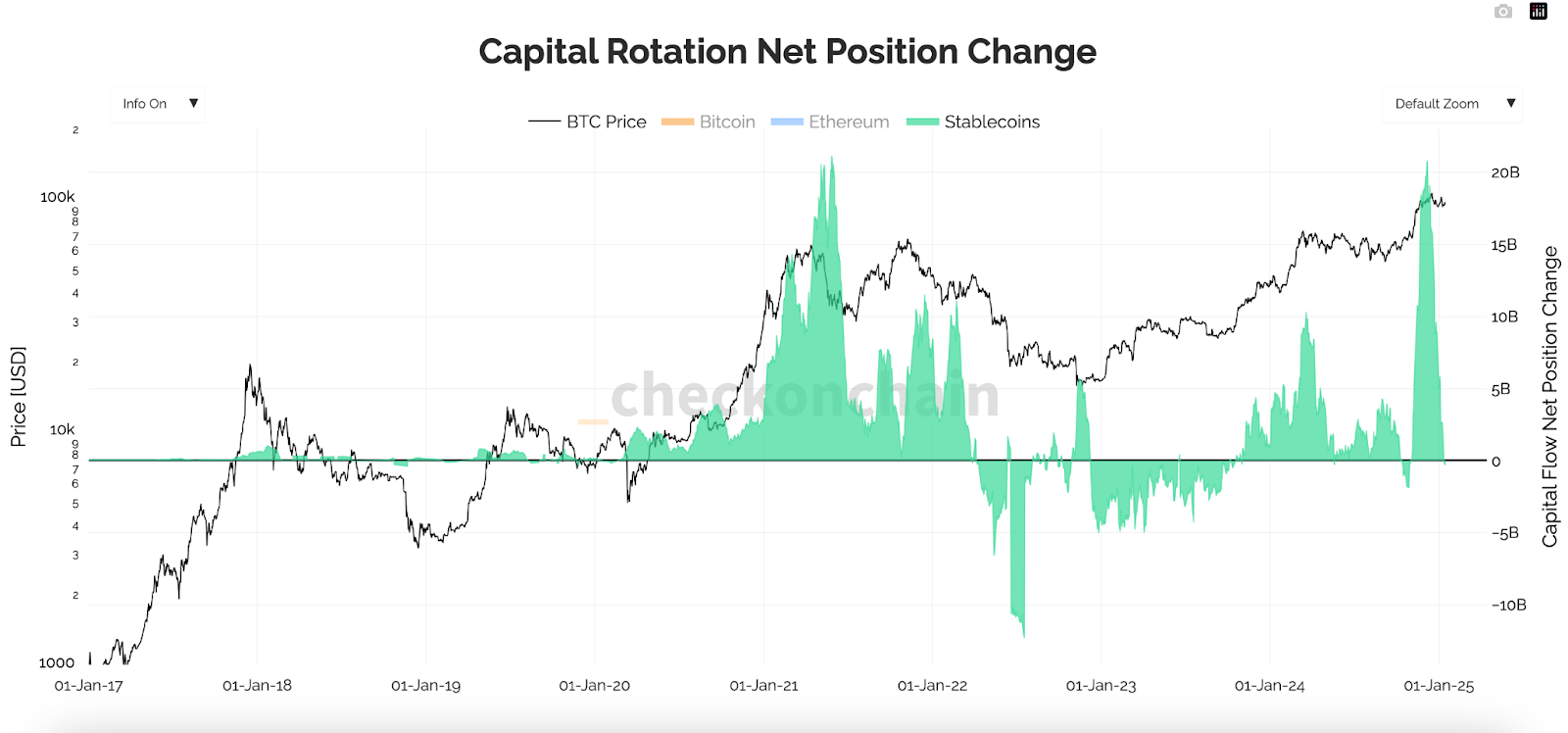

As 2024 trends show, stablecoins strengthened their infrastructural role within the crypto industry, acting as a fuel for DeFi adoption and increased crypto trading activity. Building on this expansion, the sector is well-positioned for further increase in 2025, as post-halving years are typically marked by increased trading volumes.&

The previous cycle, which became a turning point for the widespread adoption of stablecoins, indicates that their supply is likely to grow throughout much, if not all, of 2025, as capital rotation into stablecoins extended into the early bearish stages of the market. For example, stablecoin supply continued to increase until March 2022, five months after the market’s cyclical peak. Consequently, even if negative narratives hit the market, stablecoin demand may temporarily remain strong, benefiting from the trend.

During the post-halving year, the stablecoin supply increased at a relatively similar rate as a halving year, suggesting that it may reach $325 billion by the end of 2025 as a basis to support potential crypto market rally. The main variable for this year will likely be regulatory developments in the U.S. and other countries, which currently seems to be a potential amplifier that can boost stablecoin supply even further. Increased venture capital interest into stablecoin projects act as an additional catalyst that may help stablecoin supply reach the widely expected $400 billion market cap.

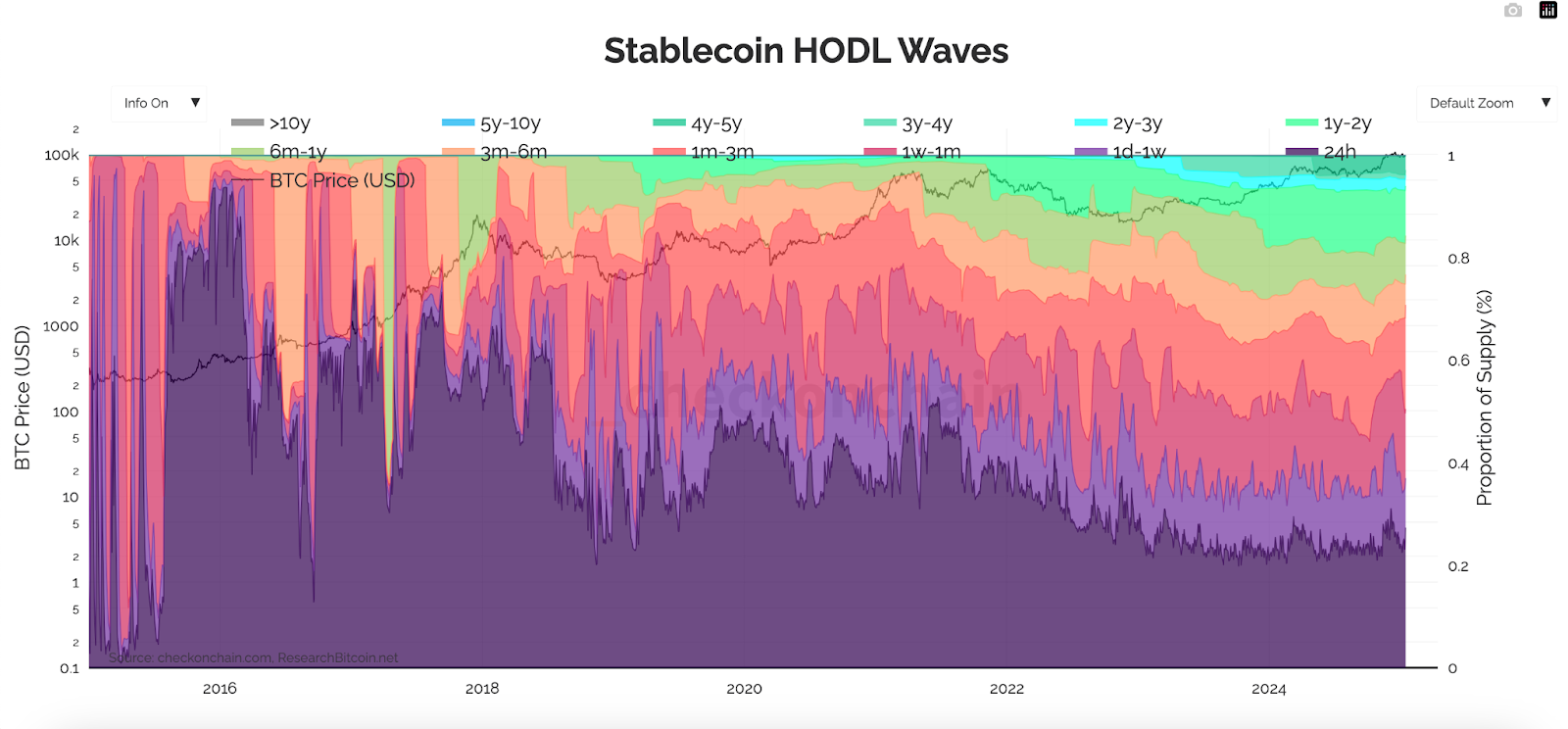

In addition to market cap expansion, post-halving years are also accompanied by heightened network activity. More than half of stablecoin supply is currently stored for less than a month, indicating high mobility of funds. Although the share of this high-mobile supply decreased from 58% to 51% in 2024, post-halving patterns suggest that stablecoin could be increasingly stored for shorter periods of time in 2025, primarily encouraged by higher on-chain trading activity.

Another trend likely to persist in 2025 is the expansion of stablecoins to non-dominant networks, primarily moving beyond Tron. The upcoming Pectra update, currently expected to launch on the mainnet in March 2025, promises scalability improvements and a more intuitive user experience with lower gas fees. These advancements could further solidify the position of Ethereum’s L1 and L2 networks as key hosts for stablecoin supply.

Meanwhile, Tron has been lagging behind Ethereum in implementing account abstraction and other user experience improvements, leaving cost-efficiency as its primary value proposition. However, as post-Dencun developments have shown, cost efficiency alone may not suffice to maintain Tron’s dominant position, as the network has been losing market share in both stablecoin supply and organic transfer volume.

Additionally, Tron’s significant reliance on USDT could pose challenges for the network. USDT’s share of the stablecoin market is already shrinking, even among fiat-backed stablecoins, and this trend is expected to continue in 2025, as the stablecoin may face headwinds due to potential regulatory disadvantages.&

For instance, Tether didn’t manage to get an e-money license to operate in the EU, while Circle obtained it in July. In addition, USDC is the only stablecoin among the top six regulated under U.S. money transmitter frameworks, giving it a compliance advantage. This regulatory edge could drive increased USDC adoption in traditional payment systems and exchange trading throughout the year. Furthermore, lower-cap stablecoins are also expected to chip away at USDT’s dominance in 2025, with new TradFi-powered stablecoins set to launch and expand their market share.

In summary, 2025 is shaping up to be a more dynamic iteration of 2024, with familiar trends continuing to evolve at a faster pace, driven by increased market diversification and the widely anticipated crypto bull run.

You can get bonuses upto $100 FREE BONUS when you:

💰 Install these recommended apps:

💲 SocialGood - 100% Crypto Back on Everyday Shopping

💲 xPortal - The DeFi For The Next Billion

💲 CryptoTab Browser - Lightweight, fast, and ready to mine!

💰 Register on these recommended exchanges:

🟡 Binance🟡 Bitfinex🟡 Bitmart🟡 Bittrex🟡 Bitget

🟡 CoinEx🟡 Crypto.com🟡 Gate.io🟡 Huobi🟡 Kucoin.

Comments