This weekly piece of cryptocurrency price analysis and thought leadership is brought to you by the expert team at CEX.IO, your crypto guide since 2013. At CEX.IO, we’re committed to providing the latest industry developments and potential price scenarios to help our users make the most informed decisions along their crypto journeys.&

In this week’s update, we discuss whether the FTX contagion could spread to other major crypto institutions following Genesis Global Capital’s recent insolvency, and how the downside price targets for Bitcoin could factor in if the current sell-off continues.

Genesis Global Capital is one of the biggest cryptocurrency lenders and has been the sole liquidity provider of Grayscale Bitcoin Trust (GBTC), the world’s largest Bitcoin trust with assets under management exceeding $10 billion.

Last week, Genesis announced that it is suspending withdrawals from its platform which naturally turned all eyes to GBTC.

In the 40th edition of the Crypto Ecosystem Update, we also discuss how Coinbase Global Inc. (COIN) hitting a new bottom in the future could also dictate the bottom for cryptocurrencies.&

Read along for in-depth breakdowns and enjoy reviews of correlated markets as we try to weather this storm together.

Could Genesis and Grayscale be the next black swans?

Digital Currency Group (DCG) owns both Genesis Capital Group and Grayscale Bitcoin Trust.&

Following FTX’s collapse, the fallout spread to Genesis, which had been bailed out by DCG back in May 2022 during Three Arrows Capital’s bankruptcy.

With Genesis’ suspending customer withdrawals last week, news began to circulate that the company could owe more than $1 billion to its creditors. And according to an article in the Wall Street Journal, the company has sought a $1 billion loan but no interest came from creditors.

Genesis’ potential insolvency has raised concerns about whether the fallout from FTX could impact Grayscale Bitcoin Trust.

To alleviate the tension, Grayscale executives declared in a tweet on November 16 that Genesis Global Capital is not a counterparty for Grayscale and that the assets underlying GBTC are stored by Coinbase in separate cold storage.

However, many people found this statement contradictory. A previous statement on October 3 from Grayscale CEO Michael Sonnenshein stated that Genesis was the company’s “sole liquidity provider.”

Thankfully, a recent filing with the U.S. Securities and Exchange Commission (SEC) could clear up the confusion. According to the filing, Genesis will no longer assist Grayscale in the distribution and marketing of the latter’s shares, but will continue to serve as a liquidity provider.

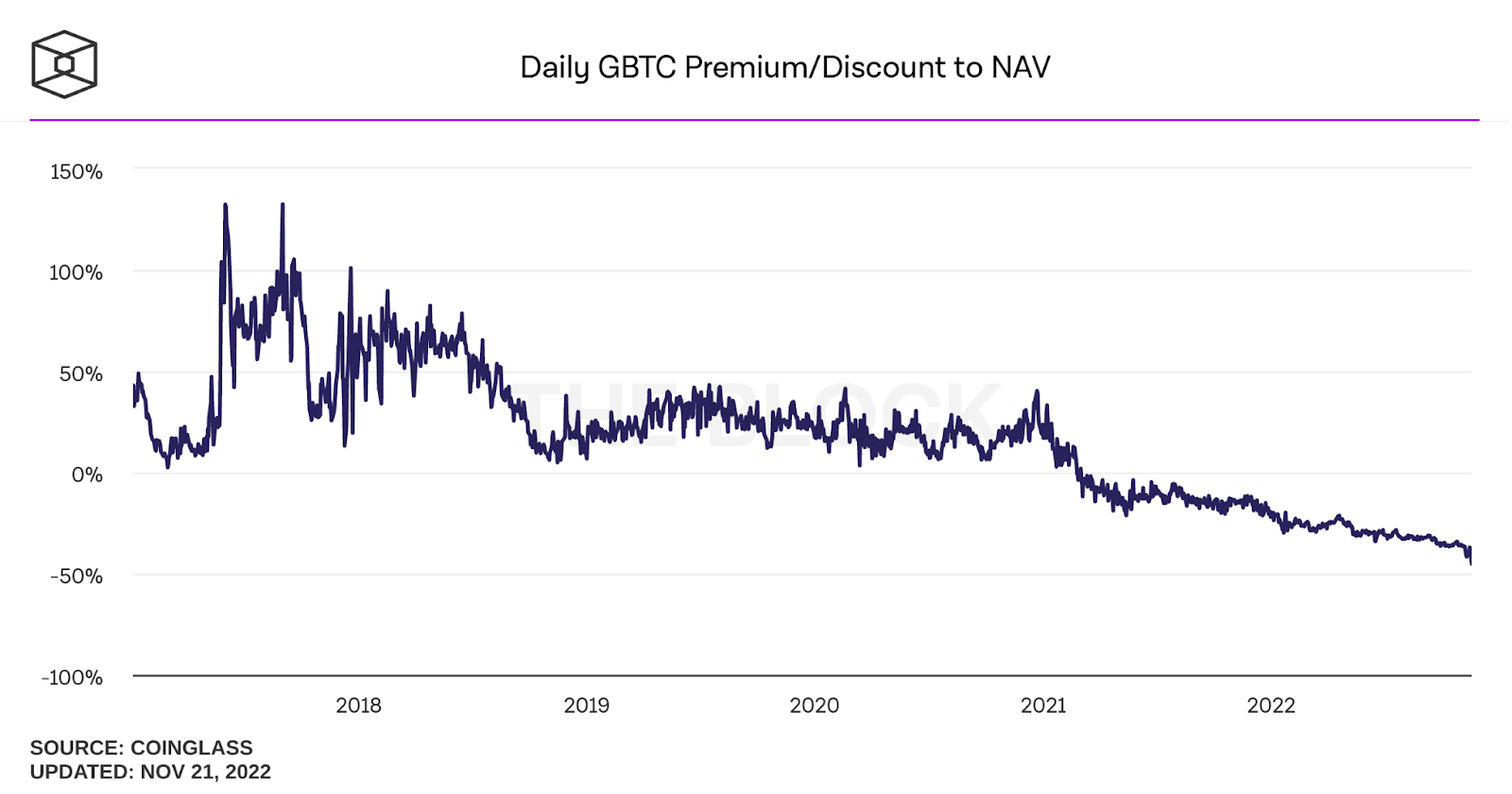

The confusion around the Genesis and Grayscale relationship was enough to push GBTC shares’ discount against the Bitcoin spot price to a record low of 43%. This means that bitcoins held under the trust are currently valued at approximately $9,000 per coin instead of the $16,000 spot price.

As indicated by the chart below, the GBTC premium has been in a death spiral since its peak in 2017.

Chart for the GBTC discount rate against Bitcoin’s spot price. Source: The Block Research.

Arthur Hayes, the former CEO of BitMEX, added fuel to the fire with a blog post on Medium that claimed the parent company Digital Currency Group had previously worked with the now-defunct trading firm Three Arrows Capital to “extract value from the GBTC premium.”

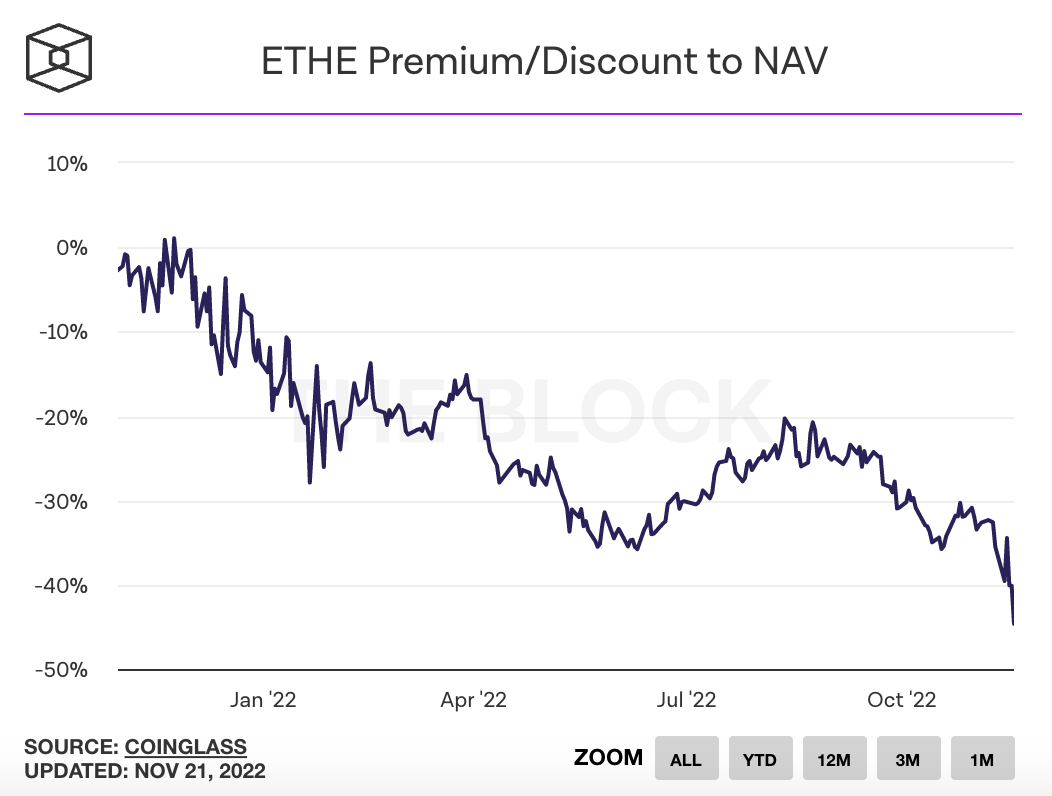

Grayscale also operates an Ethereum trust called the Grayscale Ethereum Trust (ETHE) whose shares trade at a similar discount level of 45% (see the chart below).&

ETHE discount chart relative to Ethereum’s spot price. Source: The Block Research.

Grayscale currently holds 633,400 BTC and 3.05 million ETH. The liquidation of these holdings could spell doom as it would wipe out at least $13.5 billion more in value from an already fragile ecosystem.

The ensuing panic from such a massive liquidation could have the potential to take crypto prices to new multi-year lows. Although Genesis has not yet filed for bankruptcy, news of that possibility caused BTC to drop to $15,479 – its lowest level since November 2020.&

Support levels for Bitcoin&

If the funding contagion spreads further, it could create another breakdown in cryptocurrency prices. The question for traders and analysts now is how far that capitulation could go.

In case of further capitulation, Bitcoin could backtrack to its weekly support of $14,000 from the previous cycle. That price level also corresponds to where the 400-week simple moving average is currently passing (see the chart below).

Weekly price chart for Bitcoin/U.S. dollar with the $14,000 support. Source: Tradingview.

If the $14,000 level does not hold, the next major support down the road is the $11,000 monthly support, also from the previous cycle.

You can observe in the chart below the monthly closes at $11,000 from 2018 to 2020 circled in orange, which suggests that $11,000 could indeed work as a support level if $14,000 is lost.

Monthly price chart for Bitcoin/U.S. dollar with the $11,000 support.

Finally, if none of the levels above hold, the ongoing bear flag that initiated with the breakdown from $48,000 in March could play out to its fullest with a target price of $7,777.

Flag targets are typically estimated by taking the horizontal length of a pole and extrapolating it above (for a bull flag) or below (for a bear flag) the flag’s breakout point. Considering that, the current bear flag could have $7,777 as its potential target price (see the chart below).

Target price for the bear flag coming from the $48,000 top in March.

It is of course possible for the price to bottom slightly below or above these support levels to trick out traders who have entered buy orders at those prices.

In terms of Ethereum and altcoins, their price action has been largely coupled with Bitcoin’s following the collapse of FTX as risk appetites for these assets have diminished in response to FTT and Solana’s sudden collapse.

Considering this, it could be possible for altcoin bottoms to be realized simultaneously with any potential Bitcoin bottom.&

Coinbase stock – the potential crypto bottom indicator

Another potential indicator for the crypto market bottom could be the Coinbase stock (COIN). As the ongoing negative catalyst centers around centralized exchanges, a bottom formation in the price of COIN could indicate that the contagion is over.

In that sense, when the Coinbase stock bottoms, it could also dictate the bottom prices for cryptocurrencies – unless, of course, a new and unrelated narrative joins the scene.&

The price of the Coinbase stock has been falling consistently since its public listing in April 2021, in tandem with the crypto market (see the chart below).

Coinbase stock (COIN) price progress since its public listing last year.

With this month’s dump, COIN fell back to its May 2022 low of $41 on Monday, November 21. It received a 5% bounce the next day, which also saw Bitcoin bounce from its $15,479 low (see the chart below).

COIN currently struggling to hold the $41 support from its May low.&

If the price loses the $41 floor on a weekly close, it could indicate that the current exchange contagion will continue to push Bitcoin towards the $14,000 support level or lower.

Tune in next week, and every week, for the latest CEX.IO crypto ecosystem update. For more information, head over to the Exchange to check current prices, or stop by CEX.IO University to continue expanding your crypto knowledge.

You can get bonuses upto $100 FREE BONUS when you:

💰 Install these recommended apps:

💲 SocialGood - 100% Crypto Back on Everyday Shopping

💲 xPortal - The DeFi For The Next Billion

💲 CryptoTab Browser - Lightweight, fast, and ready to mine!

💰 Register on these recommended exchanges:

🟡 Binance🟡 Bitfinex🟡 Bitmart🟡 Bittrex🟡 Bitget

🟡 CoinEx🟡 Crypto.com🟡 Gate.io🟡 Huobi🟡 Kucoin.

Comments